Table of Contents

CBSE Sample Papers for Class 12 Accountancy Solved 2016 Set 4

Part A

(Accounting for Partnership Firms and Companies)

2.What is meant by private placement of shares.

3.Rahul is admitted as a partner in M/S ABC & Co. Rahul was to bring Rs 1,00,000as goodwill. But he is not in a position to bring in the goodwill. The accountant has recorded an entry in the books of accounts by debiting goodwill account and crediting sacrificing partners’ capital account. Do you think the accountant has recorded the entry correctly? Give reasons.

4.Arun, Vijay and Raju are partners in a firm. They do not have a partnership deed.Arun and Raju have contributed a larger amount of capital as compared to Vijay and therefore, they want that the profits should be distributed in the capital ratio but Vijay did not agree. Will the claim of Arun and Raju be accepted?

5.Identify a situation for compulsory dissolution of a partnership firm?

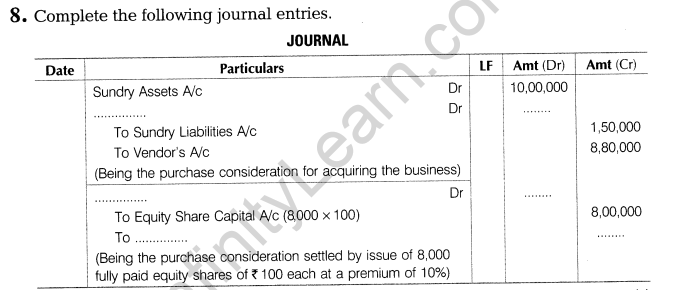

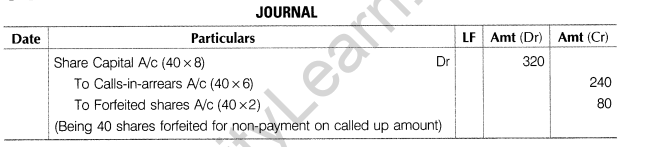

6. XYZ Ltd forfeited 40 shares of Rs 10 each 8 called-up) issued at 40% premium (payable on final call) to Ram on which he had paid 12 per share. Journalise.

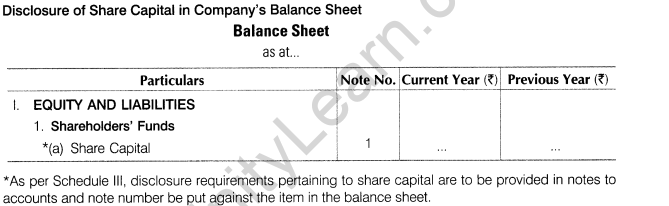

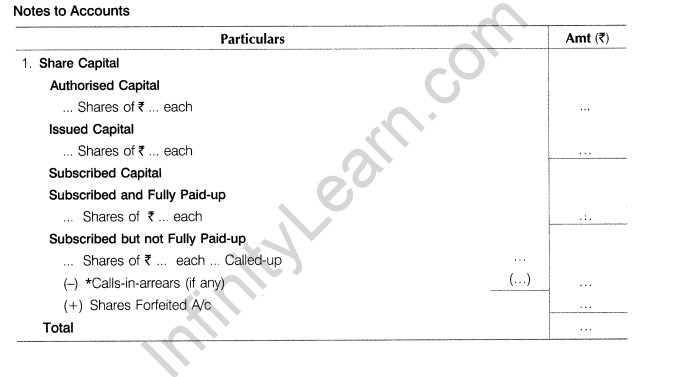

7.How will you disclose share capital in company’s balance sheet as per schedule III of the Companies Act, 2013

9.S and T are partners sharing profits and losses in the ratio of 2 : 1. U and V are admitted as partners and profit sharing ratio becomes 4 : 2 : 3 : 1. Goodwill is valued at ? 90,000. V brings in required goodwill and ? 40,000 as capital in cash. U brings in Rs 35,000 in cash and 126,000 worth stock as his capital in addition to the required amount of goodwill in cash. Show the necessary journal entries.

10.On 1st January, 2015, X Ltd received in advance the first call of ? 2 per share on 10,000 equity shares. The first call was due on 15th February, 2015.Journalise the above transactions and transfer the advance to first call account by opening calls-in-advance account.

11.Nisha and Saisha were partners. The partnership deed provided for

(i)Profits to be divided as Nisha 1/2, Saisha 1/3 and l/6th to be transferred to reserves.

(ii)The accounts are closed on 31st March each year.

(iii)In the event of the death of a partner, the executors will be entitled to

(a)Capital to the credit of the deceased partner on the date of the death.

(b)Interest on capital at 12% per annum.

(c)Proportion of profit to the date of death based on the average profits credited for the last 3 years.

(d)Share of goodwill based on three years’ purchase of the average profits of the preceding 3 years.

Additional Information

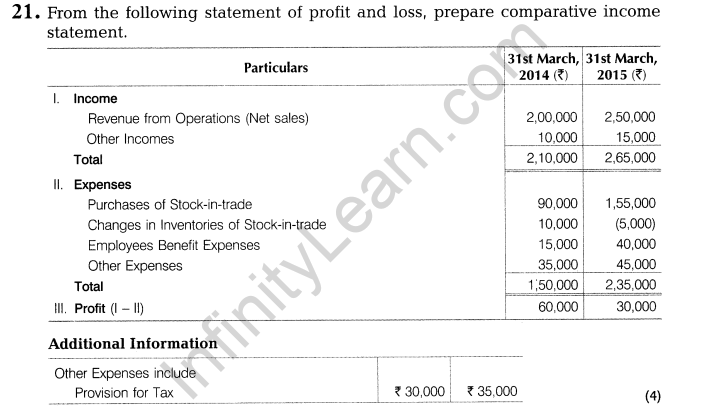

Nisha’s capital Rs 3,60,000; Saisha’s capital Rs 2,40,000; reserves Rs 90,000; cash Rs 3,30,000 and investment Rs 2,10,000.Prepare Nisha’s capital account to be presented to her executor who died on 30th April, 2015. The profits for the three precceding years were Rs 2,52,000, Rs 2,70,000 and Rs 2,97,000.

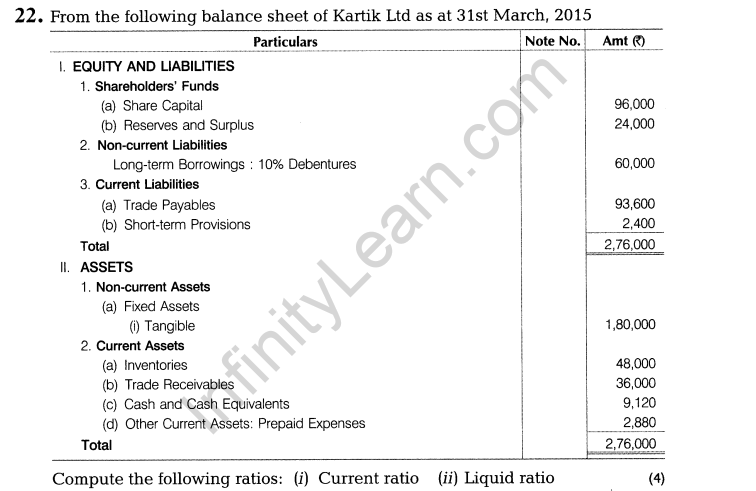

12.A and B are partners. As capital is Rs 10,000 and B’s capital is Rs 6,000. Interest is payable @ 6% per annum. B is entitled to a salary of Rs 300 per month for extra time, he devotes to the business. Profit for the current year before interest and salary to B is Rs 8,000. Divide the profit between A and B. Identify the value shown by the firm in allowing salary to B.

13.A, B and C were partners in a firm sharing profits in the ratio of 5 : 4 : 3. After division of the profits for the year ended 31st March, 2015, their capitals were Rs 5,00,000, Rs 4,00,000 and Rs 3,00,000 respectively. During the year, they withdrew Rs 30,000 each. The profit for the year was Rs 1,20,000. The partnership deed provided that interest on capital will be allowed @ 10% per annum. While preparing the final accounts, interest on capital was not allowed.

You are required to calculate the capitals as on 1st April, 2014 and pass the necessary adjustment entries for providing interest on capital. Show your working clearly. Identify the value shown by partners in correcting their mistakes.

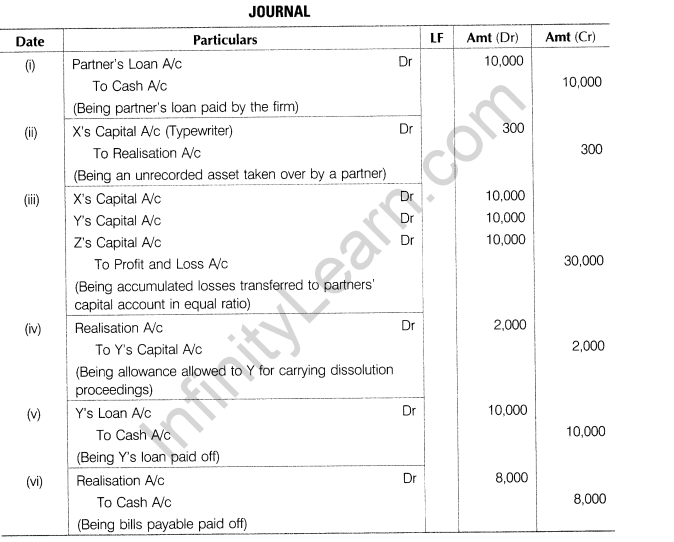

14.Pass necessary journal entries for recording the following transactions at the time of dissolution of the firm.

(i)Loan of Rs 10,000 advanced by a partner to the firm was paid on dissolution of the firm.

(ii)X, a partner takes over an unrecorded asset (typewriter) at Rs 300.

(iii) Undistributed balance (debit) of profit and loss account ? 30,000. The firm has three partners X, Y and Z.

(iv)Y who undertakes to carry out the dissolution proceedings is allowed Rs 2,000 for the same.

(v)Partner Y’s loan paid off Rs 10,000.

(vi) Rs 110,000 bills payable settled at Rs 18,000.

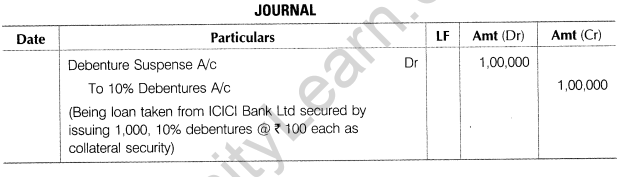

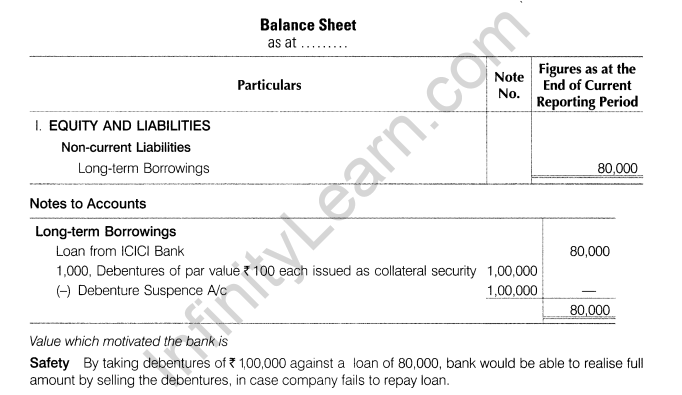

15.Mohan Ltd secured a loan of Rs 80,000 from the ICICI Bank issuing 1,000, 10% debentures of Rs 100 each as collateral security. How will be the debentures shown in the balance sheet of the company.

Identify the value, which according to you, motivated the bank, to insist for issuing debentures as collateral security against the loan.

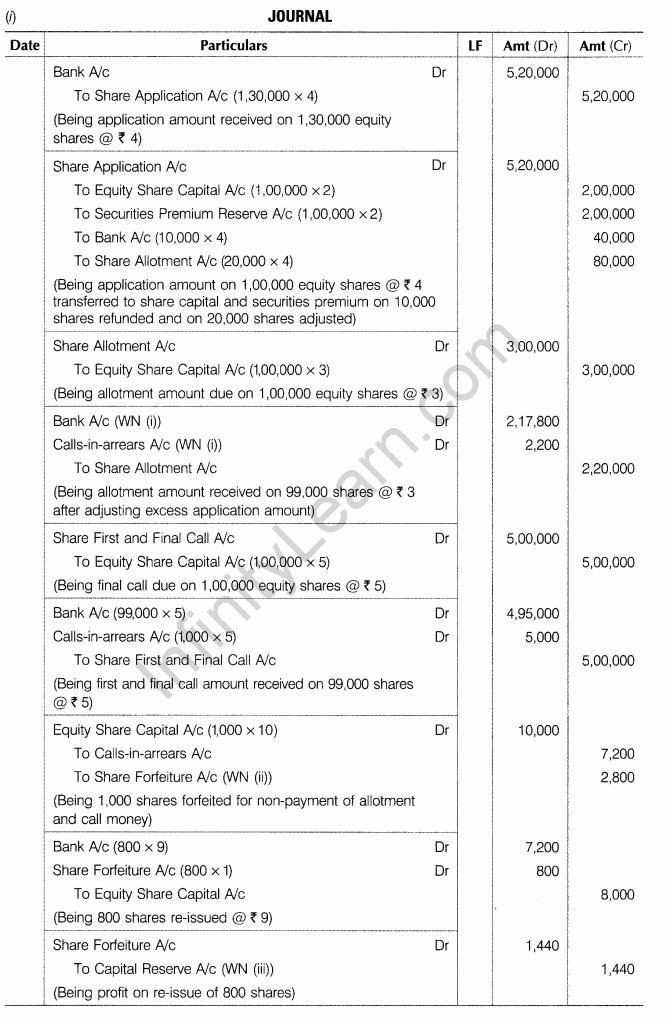

16.Makkar Ltd was registered with an authorised capital of Rs 20,00,000 in Rs 10 per equity share. It invited applications for issuing 1,00,000 equity shares at a premium of Rs 2 per share. The amount was payable as follows

On application Rs 4 per share (including premium)

On allotment Rs 3 per share

Balance on 1st and final call.

Applications were received for 1,30,000 shares. Applications for 10,000 shares were rejected and the application money received on them was refunded. Pro-rata allotment was made to the remaining applications. Amount overpaid on these applications was adjusted towards the amount due on allotment. Raj, who had applied for 1200 shares, failed to pay the allotment and call money. The company forfeited his shares, out of which 800 shares were re-issued to Mohan at X 9 per share fully paid up.

You are required to

(i)Pass the journal entries in the books of the company through calls-in-arrears account.

(ii)Prepare the share allotment account.

or

Gupta Ltd made an issue of 1,00,000 equity shares of Rs 10 each, payable as follows:

On application Rs 2.50 per share; on allotment Rs 2.50 per share and on call balance amount.

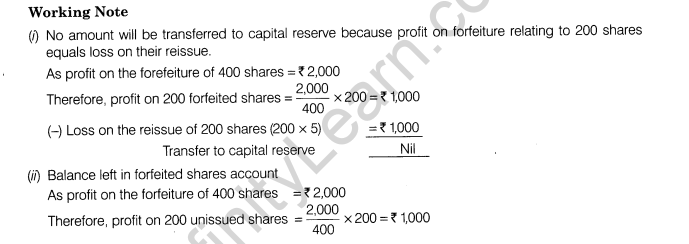

Members holding 400 shares did not pay the call money and the shares were duly forfeited. 200 of the forfeited shares were reissued as fully paid at Rs 5 per share.

Draft necessary journal entries and prepare share capital and forfeited shares accounts in the books.

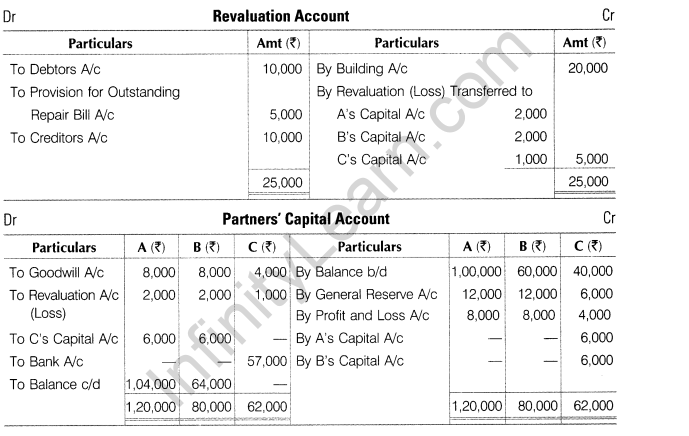

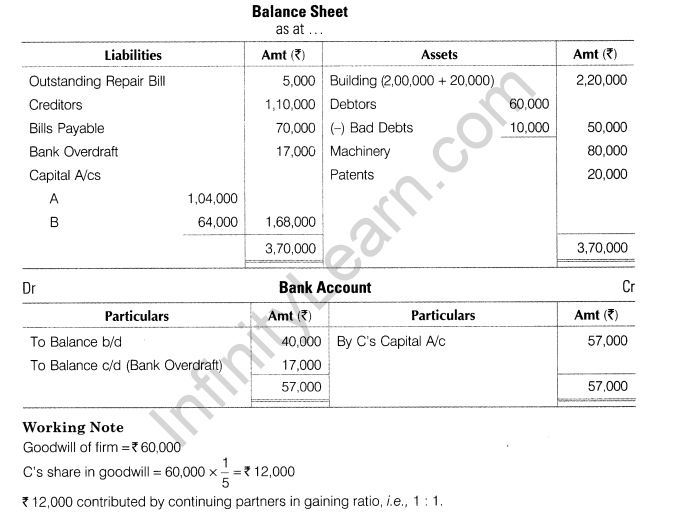

17.A, B and C are partners with 2:2:1 ratio. The following in their balance sheet:

Adjustments

(i)C takes retirement.

(ii)Goodwill of the firm is valued at Rs 60,000.

(iii)Building undervalued by Rs 20,000.

(iv)A debtor of Rs 10,000 became insolvent and nothing is receivable from him.

(v)Provision for outstanding repair bills ? 5,000.

(vi)Rs 10,000 unrecorded creditors brought into account.

(vii)A and B decide to pay off C by taking necessary bank overdraft.

Prepare revaluation account, partners’ capital account, bank account and balance sheet.

or

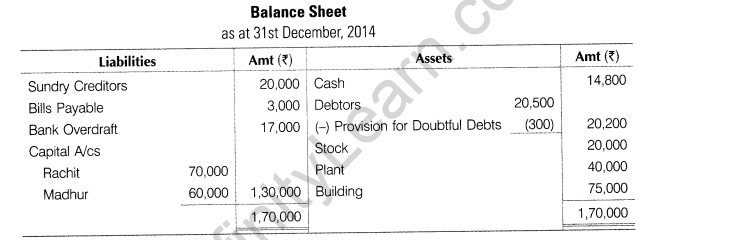

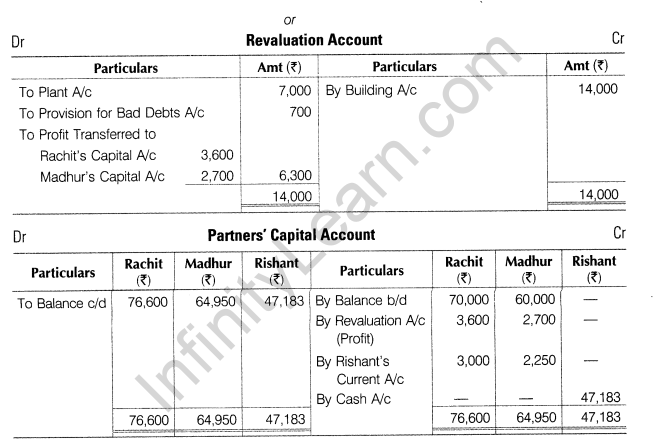

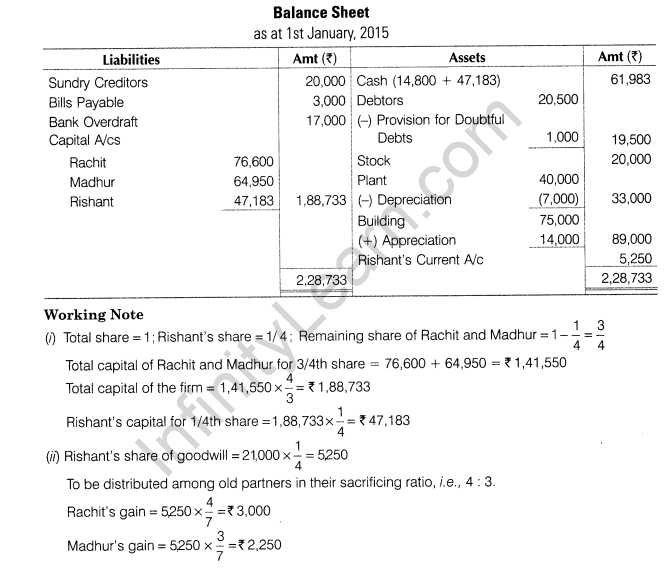

Rachit and Madhur were partners in a firm sharing profits and losses in the ratio of 4:3. The following is the balance sheet of the firm as on 31st December, 2014.

They agreed to admit Rishant as a partner with effect from 1st January, 2015 for l/4th share in profits on the following terms

(i)Rishant will bring in capital to the extent of l/4th of the total capital of the new firm after all adjustments have been made.

(ii)Building is to be appreciated by? 14,000 and plant to be depreciated by ? 7,000.

(iii)The provision on debtors is to be raised to ? 1,000.

(iv)The goodwill of the firm has been valued at ? 21,000.

Prepare revaluation account, partners’ capital account and balance sheet of the firm immediately after Rishant’s admission.

Part B

(Financial Statements Analysis)

18.The accountant of Red Chillies Ltd while preparing cash flow statement subtracted profit on sale of machinery from net profit while calculating cash flow from operating activities. Was he correct in doing so? Give reason.

19.When is interest received considered as a financing activity?

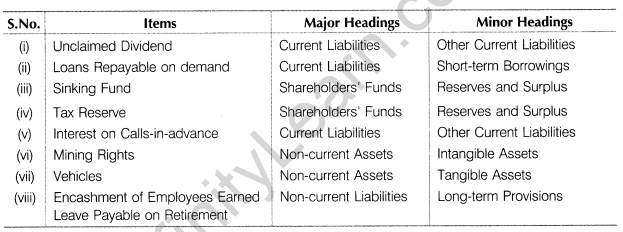

20.Under what major and minor headings will you show the following items?

(i) Unclaimed dividend (ii) Loans repayable on demand

(iii)Sinking fund (iv) Tax reserve

(v)Interest on calls-in-advance (vi) Mining rights

(vii)Vehicles

(viii) Encashment of employees earned leave payable on retirement

23.D Ltd made a profit of Rs 1,20,000 after considering the following during the year 31st March, 2015.

(i)Depreciation of fixed assets Rs 30,000.

(ii)Amortisation of goodwill Rs 20,000.

(iii)Loss on sale of machine Rs 10,000.

(iv)Profit on sale of building Rs 20,000.

(v)Transfer to general reserve Rs 30,000.

(vi)Interim dividend paid Rs 20,000.

(vii)Dividend received on investmentRs 10,000.

(viii) Provision for taxation made X 16,000.

The following additional information is also available to you

Answers

Part A

(Accounting for Partnership Firms and Companies)

Ans.

2.What is meant by private placement of shares

Ans. Private placement of shares means selling of shares to a relatively small number of selected investors and not to public in general

3.Rahul is admitted as a partner in M/S ABC & Co. Rahul was to bring Rs 1,00,000as goodwill. But he is not in a position to bring in the goodwill. The accountant has recorded an entry in the books of accounts by debiting goodwill account and crediting sacrificing partners’ capital account. Do you think the accountant has recorded the entry correctly? Give reasons.

Ans.No, the accountant has not recorded the entry correctly as it is not in accordance with Accounting Standard 26. AS-26 requires that goodwill should be recorded in the books of accounts only if money or money’s worth has been paid for it.

4.Arun, Vijay and Raju are partners in a firm. They do not have a partnership deed.Arun and Raju have contributed a larger amount of capital as compared to Vijay and therefore, they want that the profits should be distributed in the capital ratio but Vijay did not agree. Will the claim of Arun and Raju be accepted?

Ans. No, the claim of Arun and Raju will not be accepted, as in the absence of partnership deed, profits and losses are distributed among the partners equally, irrespective of their capital contribution.

5.Identify a situation for compulsory dissolution of a partnership firm?

Ans. A firm is compulsory dissolved on the insolvency of all the partners.

6. XYZ Ltd forfeited 40 shares of Rs10 each 8 called-up) issued at 40% premium (payable on final call) to Ram on which he had paid 12 per share. Journalise

Ans.

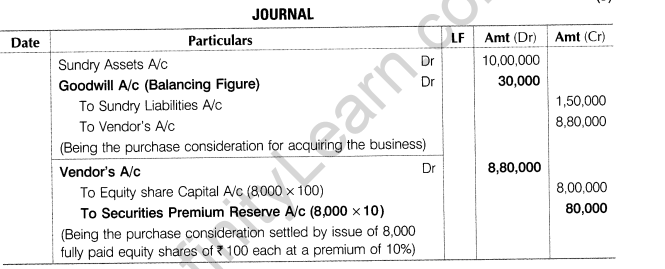

7.How will you disclose share capital in company’s balance sheet as per schedule III of the Companies Act, 2013

Ans.

Ans.

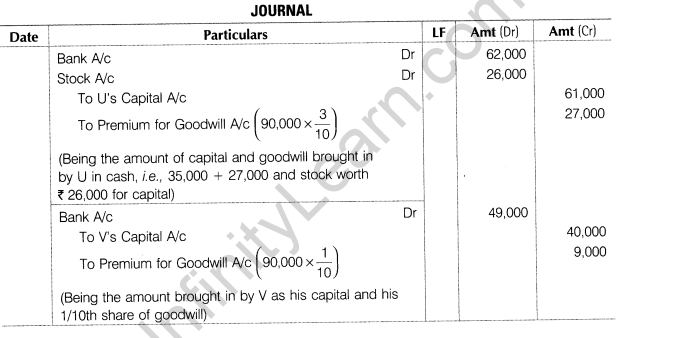

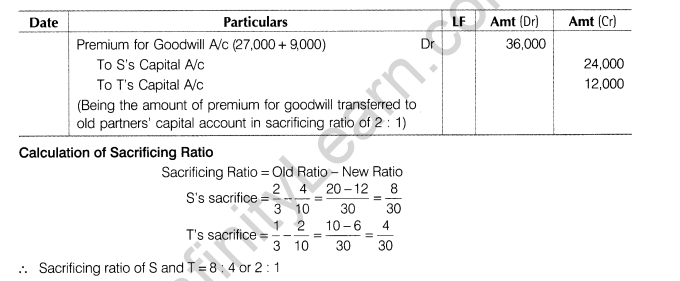

9.S and T are partners sharing profits and losses in the ratio of 2 : 1. U and V are admitted as partners and profit sharing ratio becomes 4 : 2 : 3 : 1. Goodwill is valued at ? 90,000. V brings in required goodwill and ? 40,000 as capital in cash. U brings in Rs 35,000 in cash and 126,000 worth stock as his capital in addition to the required amount of goodwill in cash. Show the necessary journal entries.

Ans.

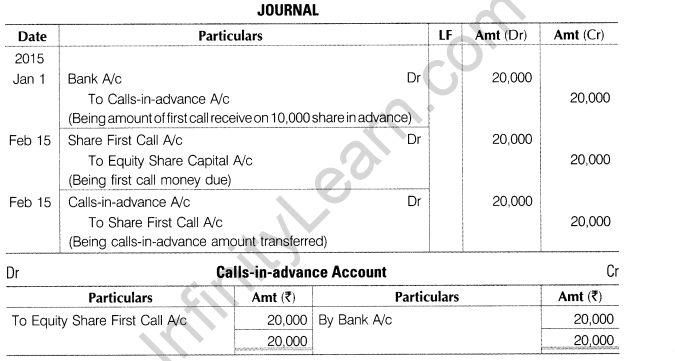

10.On 1st January, 2015, X Ltd received in advance the first call of ? 2 per share on 10,000 equity shares. The first call was due on 15th February, 2015.Journalise the above transactions and transfer the advance to first call account by opening calls-in-advance account.

Ans.

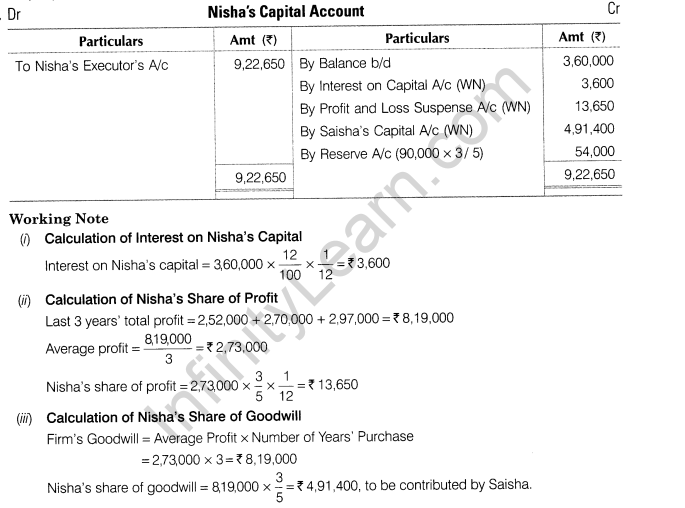

11.Nisha and Saisha were partners. The partnership deed provided for

(i)Profits to be divided as Nisha 1/2, Saisha 1/3 and l/6th to be transferred to reserves.

(ii)The accounts are closed on 31st March each year.

(iii)In the event of the death of a partner, the executors will be entitled to

(a)Capital to the credit of the deceased partner on the date of the death.

(b)Interest on capital at 12% per annum.

(c)Proportion of profit to the date of death based on the average profits credited for the last 3 years.

(d)Share of goodwill based on three years’ purchase of the average profits of the preceding 3 years.

Additional Information

Nisha’s capital Rs 3,60,000; Saisha’s capital Rs 2,40,000; reserves Rs 90,000; cash Rs 3,30,000 and investment Rs 2,10,000.Prepare Nisha’s capital account to be presented to her executor who died on 30th April, 2015. The profits for the three precceding years were Rs 2,52,000, Rs 2,70,000 and Rs 2,97,000.

Ans.

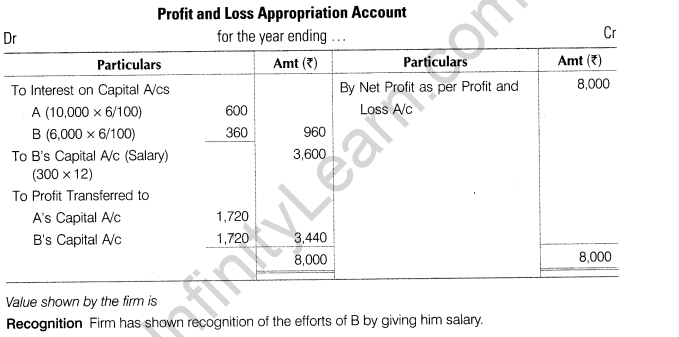

12.A and B are partners. As capital is Rs 10,000 and B’s capital is Rs 6,000. Interest is payable @ 6% per annum. B is entitled to a salary of Rs 300 per month for extra time, he devotes to the business. Profit for the current year before interest and salary to B is Rs 8,000. Divide the profit between A and B. Identify the value shown by the firm in allowing salary to B.

Ans.

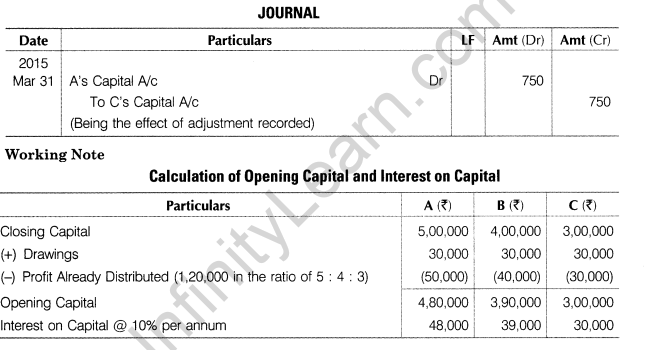

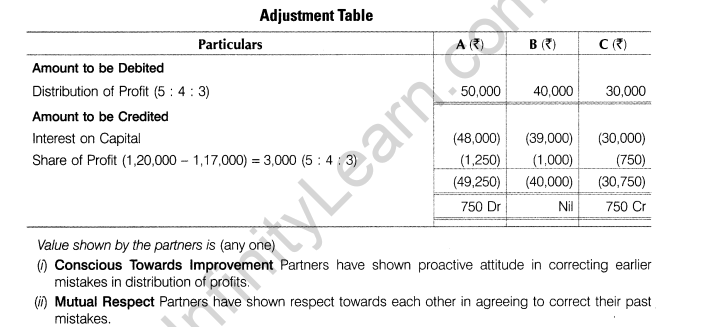

13.A, B and C were partners in a firm sharing profits in the ratio of 5 : 4 : 3. After division of the profits for the year ended 31st March, 2015, their capitals were Rs 5,00,000, Rs 4,00,000 and Rs 3,00,000 respectively. During the year, they withdrew Rs 30,000 each. The profit for the year was Rs 1,20,000. The partnership deed provided that interest on capital will be allowed @ 10% per annum. While preparing the final accounts, interest on capital was not allowed.

You are required to calculate the capitals as on 1st April, 2014 and pass the necessary adjustment entries for providing interest on capital. Show your working clearly. Identify the value shown by partners in correcting their mistakes

Ans.

14.Pass necessary journal entries for recording the following transactions at the time of dissolution of the firm.

(i)Loan of Rs 10,000 advanced by a partner to the firm was paid on dissolution of the firm.

(ii)X, a partner takes over an unrecorded asset (typewriter) at Rs 300.

(iii) Undistributed balance (debit) of profit and loss account ? 30,000. The firm has three partners X, Y and Z.

(iv)Y who undertakes to carry out the dissolution proceedings is allowed Rs 2,000 for the same.

(v)Partner Y’s loan paid off Rs 10,000.

(vi) Rs 110,000 bills payable settled at Rs 18,000.

Ans.

15.Mohan Ltd secured a loan of Rs 80,000 from the ICICI Bank issuing 1,000, 10% debentures of Rs 100 each as collateral security. How will be the debentures shown in the balance sheet of the company.

Identify the value, which according to you, motivated the bank, to insist for issuing debentures as collateral security against the loan.

Ans.

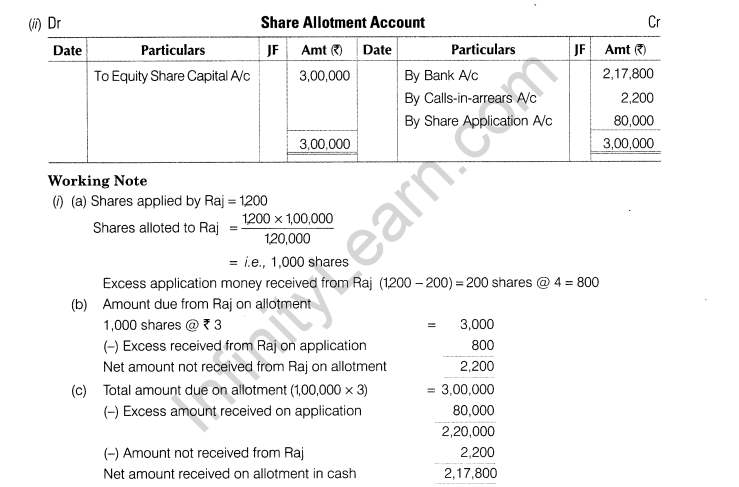

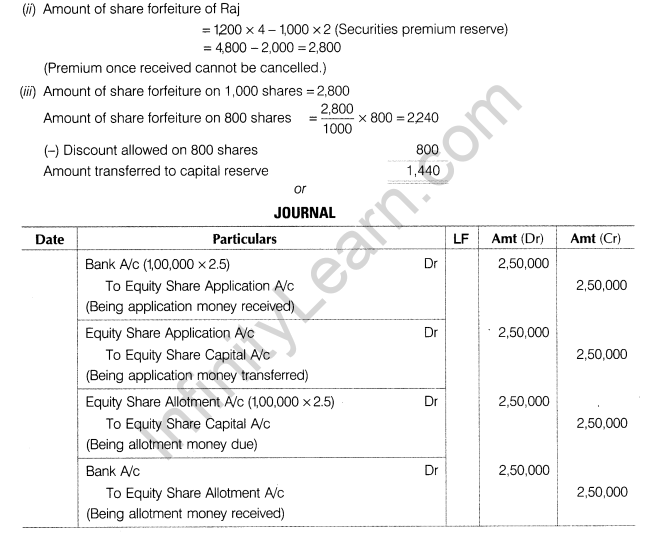

16.Makkar Ltd was registered with an authorised capital of Rs 20,00,000 in Rs 10 per equity share. It invited applications for issuing 1,00,000 equity shares at a premium of Rs 2 per share. The amount was payable as follows

On application Rs 4 per share (including premium)

On allotment Rs 3 per share

Balance on 1st and final call.

Applications were received for 1,30,000 shares. Applications for 10,000 shares were rejected and the application money received on them was refunded. Pro-rata allotment was made to the remaining applications. Amount overpaid on these applications was adjusted towards the amount due on allotment. Raj, who had applied for 1200 shares, failed to pay the allotment and call money. The company forfeited his shares, out of which 800 shares were re-issued to Mohan at X 9 per share fully paid up.

You are required to

(i)Pass the journal entries in the books of the company through calls-in-arrears account.

(ii)Prepare the share allotment account.

or

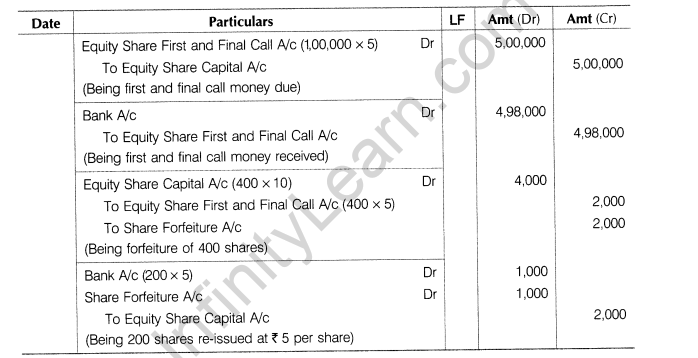

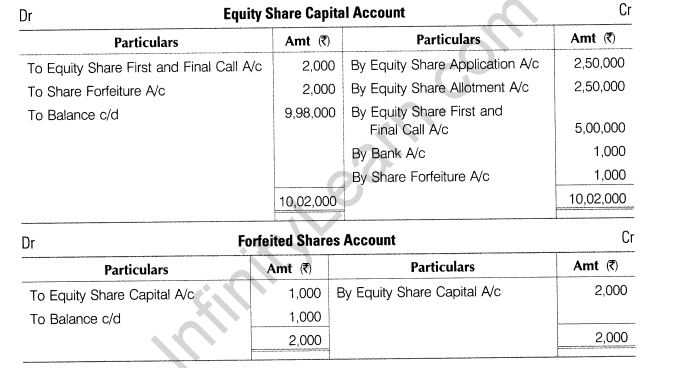

Gupta Ltd made an issue of 1,00,000 equity shares of Rs 10 each, payable as follows:

On application Rs 2.50 per share; on allotment Rs 2.50 per share and on call balance amount.

Members holding 400 shares did not pay the call money and the shares were duly forfeited. 200 of the forfeited shares were reissued as fully paid at Rs 5 per share.

Draft necessary journal entries and prepare share capital and forfeited shares accounts in the books.

Ans.

17.A, B and C are partners with 2:2:1 ratio. The following in their balance sheet:

Adjustments

(i)C takes retirement.

(ii)Goodwill of the firm is valued at Rs 60,000.

(iii)Building undervalued by Rs 20,000.

(iv)A debtor of Rs 10,000 became insolvent and nothing is receivable from him.

(v)Provision for outstanding repair bills ? 5,000.

(vi)Rs 10,000 unrecorded creditors brought into account.

(vii)A and B decide to pay off C by taking necessary bank overdraft.

Prepare revaluation account, partners’ capital account, bank account and balance sheet.

or

Rachit and Madhur were partners in a firm sharing profits and losses in the ratio of 4:3. The following is the balance sheet of the firm as on 31st December, 2014.

They agreed to admit Rishant as a partner with effect from 1st January, 2015 for l/4th share in profits on the following terms

(i)Rishant will bring in capital to the extent of l/4th of the total capital of the new firm after all adjustments have been made.

(ii)Building is to be appreciated by? 14,000 and plant to be depreciated by ? 7,000.

(iii)The provision on debtors is to be raised to ? 1,000.

(iv)The goodwill of the firm has been valued at ? 21,000.

Prepare revaluation account, partners’ capital account and balance sheet of the firm immediately after Rishant’s admission.

Ans.

Part B

(Financial Statements Analysis)

18.The accountant of Red Chillies Ltd while preparing cash flow statement subtracted profit on sale of machinery from net profit while calculating cash flow from operating activities. Was he correct in doing so? Give reason.

Ans. Yes, the treatment is correct as profit on sale of machinery is a non-operating income, it is subtracted from net profit to calculate cash flow from operating activities, while preparing cash flow statement.

19.When is interest received considered as a financing activity?

Ans. Interest received is never considered as a financing activity.

20.Under what major and minor headings will you show the following items?

(i) Unclaimed dividend (ii) Loans repayable on demand

(iii)Sinking fund (iv) Tax reserve

(v)Interest on calls-in-advance (vi) Mining rights

(vii)Vehicles

(viii) Encashment of employees earned leave payable on retirement

Ans.

Ans.

Ans.

23.D Ltd made a profit of Rs 1,20,000 after considering the following during the year 31st March, 2015.

(i)Depreciation of fixed assets Rs 30,000.

(ii)Amortisation of goodwill Rs 20,000.

(iii)Loss on sale of machine Rs 10,000.

(iv)Profit on sale of building Rs 20,000.

(v)Transfer to general reserve Rs 30,000.

(vi)Interim dividend paid Rs 20,000.

(vii)Dividend received on investmentRs 10,000.

(viii) Provision for taxation made X 16,000.

The following additional information is also available to you

Ans.