Banking – CBSE Notes for Class 12 Macro Economics

Introduction:

This is a textual description of commercial bank, credit creation by commercial bank, central bank and its functions.

Commercial Bank And Credit Creation By Commercial Bank

1. Commercial bank is a financial institution which performs the functions of accepting deposits from the public and making loans and investments, with the motive of earning profit.

2. Process of money creation/deposit creation/credit creation by the commercial banking system.

(a) Let us assume that the entire commercial banking system is one unit. Let us call this one unit simply “banks’. Let us also assume that all receipts and payments in the economy are routed through the banks. One who makes payment does it by writing cheque. The one who receives payment deposits the same in his deposit account.

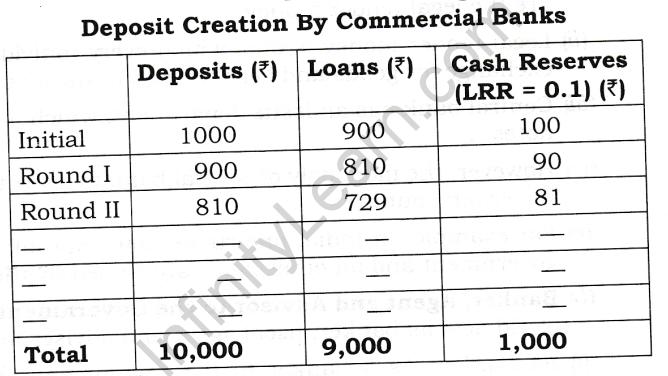

(b) Suppose initially people deposit Rs.1000. The banks use this money for giving loans. But the banks cannot use the whole of deposit for this purpose. It is legally compulsory for the banks to keep a certain minimum fraction of these deposits as cash. The fraction is called the Legal Reserve Ratio (LRR). The LRR is fixed by the Central Bank. It has two components. A part of the LRR is to be kept with the Central bank and this part ratio is called the Cash Reserve Ratio. The other part is kept by the banks with themselves and is called the Statutory Liquidity Ratio.

(c) Let us now explain the process, suppose the initial deposits in banks is Rs.1000 and the LRR is 10 percent. Further, suppose that banks keep only the minimum required, i.e., Rs.100 as cash reserve, banks are now free to lend the remainder Rs.900. Suppose they lend Rs.900. What banks do to open deposit accounts in the names of the borrowers who are free to withdraw the amount whenever they like.

• Suppose they withdraw the whole of amount for making payments.

(d) Now, since all the transactions are routed through the banks, the money spent by the borrowers comes back into the banks into the deposit accounts of those who have received this payment. This increases demand deposit in banks by ?900. It is 90 per cent of the initial deposit. These deposits of Rs.900 have resulted on account

of loans given by the banks. In this sense the banks are responsible for money creation. With this round, increased in total deposits are now Rs.1900 (=1000 + 900).

(e) When banks receive new deposit of ?900, they keep 10 per cent of it as cash reserves and use the remaining Rs. 810 for giving loans. The borrowers use these loans for making payments. The money comes back into the accounts of those who have received the payments. Bank deposits again rise, but by a smaller amount of Rs.810. It is 90 per cent of the last deposit creation. The total deposits now increase to Rs.2710 (=1000 + 900 + 810). The process does not end here.

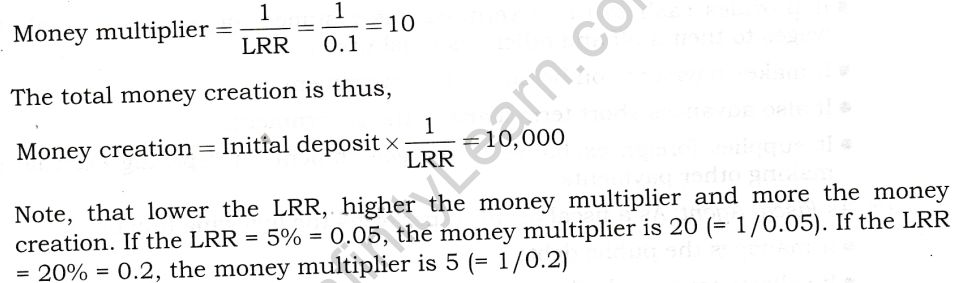

(f) The deposit creation continues in the above manner. The deposits go on increasing round after round but Deposit Creation By Commercial Banks each time only 90 per cent of the last round deposits. At the same time cash reserves go on increasing, each time 90 per cent of the last cash reserve. The deposit creation comes to end when the total cash reserves become equal to the initial deposit. The total deposit creation comes to Rs.10000, ten times the initial deposit as shown in the table.

It can also be explained with the help of the following formula:

3. Banks required to keep only a fraction of deposits as cash reserves Banks are required to keep only a fraction of deposits as cash reserves because of the following two reasons:

(a) First, the banking experience has revealed that not all depositors approach the banks for withdrawal of money at the same time and also that normally they withdraw a fraction of deposits.

(b) Secondly, there is a constant flow of new deposits into the banks. Therefore to meet the daily demand for withdrawal of cash, it is sufficient for banks to keep only a fraction of deposits as a cash reserve.

4. When the primary cash deposit in the banking system leads to multiple expansion in the total deposits, it is known as money multiplier or credit multiplier.

Central Bank And Their Functions

1. The central bank is the apex institution of a country’s monetary system. The design and the control of the country’s monetary policy is its main responsibility. India’s central bank is the Reserve Bank of India.

2. Functions of Central Bank.

(a) Currency Authority:

(i) The central bank has the sole monopoly to issue currency notes. Commercial banks cannot issue currency notes. Currency notes issued by the central bank are the legal tender money.

(ii) Legal tender money is one, which every individual is bound to accept by law in exchange for goods and services and in the discharge of debts.

(iii) Central bank has an issue department, which is solely responsible for the issue of notes.

(iv) However, the monopoly of central bank to issue the currency notes may be partial in certain countries.

(v) For example, in India, one rupee notes and all types of coins are issued by the government and all other notes are issued by the Reserve Bank of India.

(b) Banker, Agent and Advisor to the Government: Central bank everywhere in the world acts as banker, fiscal agent and adviser to their respective government.

(i) As Banker: As a banker to the government, the central bank performs same functions as performed by the commercial banks to their customers.

• It receives deposits from the government and collects cheques and drafts deposited in the government account.

• It provides cash to the government as resumed for payment of salaries and wages to their staff and other cash disbursements.

• It makes payments on behalf of the government.

• It also advances short term loans to the government.

• It supplies foreign exchange to the government for repaying external debt or making other payments.

(ii) As Fiscal Agent: As a fiscal agent, it performs the following functions :

• It manages the public debt.

• It collects taxes and other payments on behalf of the government.

• It represents the government in the international financial institutions (such as World Bank, International Monetary Fund, etc.) and conferences.

(iii) As Adviser

• The central bank also acts as the financial adviser to the government.

• It gives advice to the government on all financial and economic matters such as deficit financing, devaluation of currency, trade policy, foreign exchange policy, etc.

3. Banker’s Bank and Supervisor:

(a) Banker’s Bank: Central bank acts as the banker to the banks in three ways: (i) custodian of the cash reserves of the commercial banks; (ii) as the lender of the last resort; and (iii) as clearing agent.

(i) As a custodian of the cash reserves of the commercial banks, the central bank maintains the cash reserves of the commercial banks. Every commercial bank has to keep a certain percent of its cash reserves with the central bank by law.

(ii) As Lender of the Last Resort.

• As banker to the banks, the central bank acts as the lender of the last resort.

• In other words, in case the commercial banks fail to meet their financial requirements from other sources, they can, as a last resort, approach to the central bank for loans and advances.

• The central bank assists such banks through discounting of approved securities and bills of exchange.

(ii) As Clearing Agent

• Since it is the custodian of the cash reserves of the commercial banks, the central bank can act as the clearinghouse for these banks.

• Since all banks have their accounts with the central bank, the central bank can easily settle the claims of various banks against each other simply by book entries of transfers from and to their accounts.

• This method of settling accounts is called Clearing House Function of the central bank.

(b) Supervisor

(i) The Central Bank supervises, regulate and control the commercial banks.

(ii) The regulation of banks may be related to their licensing, branch expansion, liquidity of assets, management, amalgamation (merging of banks) and liquidation (the winding of banks).

(iii) The control is exercised by periodic inspection of banks and the returns filed by them.

4. Controller of Money Supply and Credit: Principal instruments of Monetary Policy or credit control of the Central Bank of a country are broadly classified as:

(a) Quantitative Instruments or General Tools; and

(b) Qualitative Instruments or Selective Tools.

(a) Quantitative Instruments or General Tools of Monetary Policy: These are the instruments of monetary policy that affect overall supply of money/credit in the economy. These instruments do not direct or restrict the flow of credit to some specific sectors of the economy. They are as under:

(i) Bank Rate (Discount Rate)

• Bank rate is the rate of interest at which central bank lends to commercial banks without any collateral (security for purpose of loan). The thing, which has to be remembered, is that central bank lends to commercial banks and not to general public.

• In a situation of excess demand leading to inflation,

-> Central bank raises bank rate that discourages commercial banks in borrowing from central bank as it will increase the cost of borrowing of commercial bank.

-> It forces the commercial banks to increase their lending rates, which discourages borrowers from taking loans, which discourages investment.

-> Again high rate of interest induces households to increase their savings by restricting expenditure on consumption.

-> Thus, expenditure on investment and consumption is reduced, which will control the excess demand.

• In a situation of deficient demand leading to deflation,

-> Central bank decreases bank rate that encourages commercial banks in borrowing from central bank as it will decrease the cost of borrowing of commercial bank.

-> Decrease in bank rate makes commercial bank to decrease their lending rates, which encourages borrowers from taking loans, which encourages investment.

-> Again low rate of interest induces households to decrease their savings by increasing expenditure on consumption.

-> Thus, expenditure on investment and consumption increase, which will control the deficient demand.

(ii) Repo Rate

• Repo rate is the rate at which commercial bank borrow money from the central

bank for short period by selling their financial securities to the central bank.

• These securities are pledged as a security for the loans.

• It is called Repurchase rate as this involves commercial bank selling securities

to RBI to borrow the money with an agreement to repurchase them at a later

date and at a predetermined price.

• So, keeping securities and borrowing is repo rate.

• In a situation of excess demand leading to inflation,

-> Central bank raises repo rate that discourages commercial banks in borrowing from central bank as it will increase the cost of borrowing of commercial bank.

-> It forces the commercial banks to increase their lending rates, which discourages borrowers from taking loans, which discourages investment.

-> Again high rate of interest induces households to increase their savings by restricting expenditure on consumption.

-> Thus, expenditure on investment and consumption is reduced, which will control the excess demand.

• In a situation of deficient demand leading to deflation,

-> Central bank decreases Repo rate that encourages commercial banks in borrowing from central bank as it will decrease the cost of borrowing of commercial bank.

-> Decrease in Repo rate makes commercial bank to decrease their lending rates, which encourages borrowers from taking loans, which encourages investment.

-> Again low rate of interest induces households to decrease their savings by increasing expenditure on consumption.

-> Thus, expenditure on investment and consumption increase, which will control the deficient demand.

(iii) Reverse Repo Rate

• It is the rate at which the Central Bank (RBI) borrows money from commercial bank.

• In a situation of excess demand leading to inflation, Reverse repo rate is increased, it encourages the commercial bank to park their funds with the central bank to earn higher return on idle cash. It decreases the lending capability of commercial banks, which controls excess demand.

• In a situation of deficient demand leading to deflation, Reverse repo rate is decreased, it discourages the commercial bank to park their funds with the central bank. It increases the lending capability of commercial banks, which controls deficient demand.

(iv) Open Market Operations (OMO)

• It consists of buying and selling of government securities and bonds in the open market by Central Bank.

• In a situation of excess demand leading to inflation, central bank sells government securities and bonds to commercial bank. With the sale of these securities, the power of commercial bank of giving loans decreases, which will control excess demand.

• In a situation of deficient demand leading to deflation, central bank purchases

government securities and bonds from commercial bank. With the purchase of these securities, the power of commercial bank of giving loans increases, which will control deficient demand.

(v) Varying Reserve Requirements

• Banks are obliged to maintain reserves with the central bank, which is known as legal reserve ratio. It has two components. One is the Cash Reserve Ratio or CRR and the other is the SLR or Statutory Liquidity Ratio.

• Cash Reserve Ratio:

-> It refers to the minimum percentage of a bank’s total deposits, which it is required to keep with the central bank. Commercial banks have to keep with the central bank a certain percentage of their deposits in the form of cash reserves as a matter of law.

-> For example, if the minimum reserve ratio is 10% and total deposits of a certain bank is Rs. 100 crore, it will have to keep Rs. 10 crore with the Central Bank.

-> In a situation of excess demand leading to inflation, Cash Reserve Ratio (CRR) is raised to 20 per cent, the bank will have to keep Rs.20 crore with the Central Bank, which will reduce the cash resources of commercial bank and reducing credit availability in the economy, which will control excess demand.

-> In a situation of deficient demand leading to deflation, cash reserve ratio (CRR) falls to 5 per cent, the bank will have to keep Rs. 5 crore with the central bank, which will increase the cash resources of commercial bank and increasing credit availability in the economy, which will control deficient demand.

(vi) The Statutory Liquidity Ratio (SLR)

• It refers to minimum percentage of net total demand and time liabilities, which commercial banks are required to maintain with themselves.

• In a situation of excess demand leading to inflation, the central bank increases statutory liquidity ratio (SLR), which will reduce the cash resources of commercial bank and reducing credit availability in the economy.

• In a situation of deficient demand leading to deflation, the central bank decreases statutory liquidity ratio (SLR), which will increase the cash resources of commercial bank and increases credit availability in the economy.

• It may consist of:

-> Excess reserves

-> Unencumbered (are not acting as security for loans from the Central Bank) government and other approved securities (securities whose repayment is guaranteed by the government); and

-> Current account balances with other banks.

(b) Qualitative Instruments or Selective Tools of Monetary Policy: These

instruments are used to regulate the direction of credit. They are as under:

(i) Imposing margin requirement on secured loans

• Business and traders get credit from commercial bank against the security of their goods. Bank never gives credit equal to the full value of the security. It always pays less value than the security.

• So, the difference between the value of security and value of loan is called

marginal requirement.

• In a situation of excess demand leading to inflation, central bank raises marginal requirements. This discourages borrowing because it makes people gets less credit against their securities.

• In a situation of deficient demand leading to deflation, central bank decreases marginal requirements. This encourages borrowing because it makes people get more credit against their securities.

(ii) Moral Suasion

• Moral suasion implies persuasion, request, informal suggestion, advice and appeal by the central banks to commercial banks to cooperate with general monetary policy of the central bank.

• In a situation of excess demand leading to inflation, it appeals for credit contraction.

• In a situation of deficient demand leading to deflation, it appeals for credit expansion.

(iii) Selective Credit Controls (SCCs)

• In this method the central bank can give directions to the commercial banks not to give credit for certain purposes or to give more credit for particular purposes or to the priority sectors.

• In a situation of excess demand leading to inflation, the central bank introduces rationing of credit in order to prevent excessive flow of credit, particularly for speculative activities. It helps to wipe off the excess demand.

• In a situation of deficient demand leading to deflation, the central bank withdraws rationing of credit and make efforts to encourage credit.

Words that Matter

1. Commercial Bank: Commercial bank is a financial institution which performs the functions of accepting deposits from the public and making loans and investments, with the motive of earning profit.

2. Legal Reserve Ratio: It is the minimum ratio of deposits legally required to be kept by the commercial banks with themselves (Statutory Liquidity Ratio) and with the central bank (Cash reserve Ratio).

3. Money Multiplier or Credit Multiplier: When the primary cash deposit in the banking system leads to multiple expansion in the total deposits, it is known as money multiplier or credit multiplier.

4. Central Bank: The central bank is the apex institution of a country’s monetary system. The design and the control of the country’s monetary policy is its main responsibility.

5. Quantitative Instruments or General Tools of Monetary Policy: These are the instruments of monetary policy that affect overall supply of money/credit in the economy.

6. Qualitative Instruments or Selective Tools of Monetary Policy: The instruments which are used to regulate the direction of credit is known as Qualitative Instruments.

7. Bank rate: It is the rate of interest at which central bank lends to commercial banks without any collateral (security for purpose of loan).

8. Repo rate: It is the rate at which commercial bank borrow money from the central bank for short period by selling their financial securities to the central bank.

9. Reverse Repo rate: It is the rate at which the central bank (RBI) borrows money from commercial bank.

10. Open Market Operation: It consists of buying and selling of government securities and bonds in the open market by central bank.

11. Cash Reserve Ratio: It refers to the minimum percentage of a bank’s total deposits, which it is required to keep with the central bank.

12. Statutory Liquidity Ratio: It refers to minimum percentage of net total demand and time liabilities, which commercial banks are required to maintain with themselves.

13. Marginal requirement: Business and traders get credit from commercial bank against the security of their goods. Bank never gives credit equal to the full value of the security. It always pays less value than the security. So, the difference between the value of security and value of loan is called marginal requirement.

14. Moral suasion: It implies persuasion, request, informal suggestion, advice and appeal by the central banks to commercial banks to cooperate with general monetary policy of the central bank.

15. Selective Credit Controls (SCCs): In this method the central bank can give directions to the commercial banks not to give credit for certain purposes or to give more credit for particular purposes or to the priority sectors.