Introduction to Economics – CBSE Notes for Class 12 Micro Economics

Introduction

This chapter primarily deals with the Economy, Central problem of an economy and explains the production possibility Frontier along with their shapes, pertaining to the subject. It highlights introduction to economics and its branches, namely Microeconomics and Macroeconomics.

A Simple Economy

1. Society consists of people and people in the society need many goods and services in their everyday life including food, clothing, shelter, transport facilities like, roads, railways and various other services like that of teachers and doctors.

2. In fact, the list of goods and services that any individual need is so large that no individual in society, to begin with, has all the things he needs.

3. For example, the teacher in the school has the skills required to impart education to the students and he can earn some money by teaching students in the school and use the money for obtaining the goods and services that he wants.

4. Economy is a system which provides people with the means to work and earn a living.

5. Economics is about studying economic problems arising due to limited means (having alternative uses) in relation to unlimited wants.

6.

- Economic problem is a problem of choice involving satisfaction of unlimited wants out of limited resources having alternative uses.

- Take an example of a piece of land. It can be used for constructing a house, a factory, a school, a park etc. It can also be used for growing wheat, rice, vegetables etc. The economic problem here is that for which purpose this piece of land should be used.

- Similar problems may arise in making a choice in the use of other resources like labour, capital and enterprise.

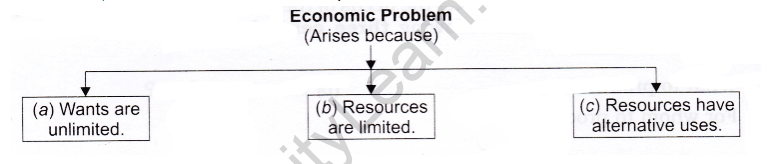

7. Economic problem arises because of scarcity of resources in relation to demand for them.

- Wants are unlimited:

- This is a basic fact of human life.

Human wants are unlimited. - They are not only unlimited but also grow and multiply veiy fast.

- This is a basic fact of human life.

- Resources are limited:

- The resources to produce goods and services to satisfy human wants are available in limited quantities. Land, labour, capital and enterprise are the basic scarce resources.

- These resources are available in limited quantities in every economy, big or small, developed or underdeveloped, rich or poor. Some economies may have more of one or two resources but not all the resources.

- For example, Indian economy has relatively more labour but less capital and land. The U.S. economy has relatively more land but less labour. No economy in the world is rich in all the resources.

- Resources have alternative uses:

- Generally a resource has many alternative uses.

- A worker can be employed in a factory, in a school, in a government office, self employed and so on.

- Like this, nearly all resources have alternative uses. But the problem is that which resource should be put to which use.

8. “Scarcity” in economics is the short supply of resources in relation to the demand. Resources of the economy are scarce with the result that the economy can’t produce all that the society needs.

- Greater Scarcity Higher Prices

Examples: Petrol, Diamonds - Lesser Scarcity Lesser Prices

Example: Water - No Scarcity No Price

Example: Air we breathe

9. Economising of resources means that resources are to be used in such a manner that the maximum output is realised per unit of input. It also means optimum utilization of resources.

Central Problems Of An Economy

1. The problem of making a choice among alternative uses of resources is known as basic or central problem of an economy.

2. There are many central problems of an economy, but according to syllabus we have to do one, that is;

Problem of Allocation of Resources: Every economy has limited resources which can alternatively be used to produce different goods and services. Hence, it has to allocate its available resources in the production of different goods and services in such a manner that it ideally meets the needs of the society. While allocating resources optimally, the decisions the following three central problems of an economy are required to be taken:

- What to produce?

- How to produce?

- For whom to produce?

(a) What to produce?

- What to produce refers to a problem in which decision regarding which goods and services should be produced is to be taken.

- Since its resources are limited, every economy has to decide what commodities are to be produced and in what quantities.

- In view of limited resources when we produce more of a commodity, it means we will be able to produce less of another. Because more production of one commodity would force us to withdraw resources from the production of the other commodity.

- So, the economy has to choose between capital goods (like machines, tools, etc.), civil goods (like cloth, watch, radio etc.), consumer goods (like wheat, cloth, shoes, sugar, etc.), military goods (like guns, bombs, tanks, etc.) necessities of life (such as food, clothing, housing, etc.) and luxury goods (such as car, colour TV, etc).

- The guiding principle for an economy here is to allocate resources in such a way that gives maximum aggregate utility to the society.

(b) How to produce?

- How to produce refers to a problem in which decision regarding which technique of production should be used is taken.

- Goods and services can be produced in two ways: by using labour intensive techniques, and by using capital-intensive techniques.

- Under labour intensive techniques, more of labour and less of capital per unit of output is used in producing goods and services, while in capital-intensive techniques more of capital and less of labour per unit of output is used.

- Thus, the economy has to decide whether the chosen goods and services should be produced with the help of automatic machines or handicrafts. Every method of production has its own advantages and disadvantages.

- For example, on one side use of more capital; i.e., automatic machines, increases the quantity and improves the quality of production but it results in unemployment as it requires lesser number of labourers. On the other side, handicrafts generate more employment but produce smaller amount of production.

- The guiding principle for an economy in such a case is to decide about the techniques of production on the basis of cost of production. Those techniques of production should be used which lead to the least possible cost per unit of commodity or service.

(c) For whom to produce?

- For whom to produce refers to a problem in which decision regarding which category of people are going to consume a good, i.e., economically poor or rich.

- As we know, goods and services are produced for those who can purchase them or have the capacity to buy them.

- Capacity to buy depends upon how income is distributed among the factors of production. The higher the income, the higher will be the capacity to buy and vice Versa. So, this is a problem of distribution.

- We know that the whole output is distributed among factors of production which have contributed to it.

- Since production is the combined efforts of all the four factors of production, viz, land, labour, capital and enterprise, it is distributed among them in the form of money income (i.e. rent, wages, interest and profits). Who should get how much is, thus, the problem.

- The guiding principle is that the economy must see here that important and urgent wants of its citizens are being satisfied to the maximum possible extent or not.

Production Possibility Frontier

1. Production possibility frontier is a curve which depicts all possible combinations of two goods which can be produced with given resources and technology in an economy.

2. Production possibility frontier is also known as production possibility curve or transformation curve.

3. The concept of PP curve is based on the following assumptions:

- First, the amount of resources in the economy is fixed.

- Second, the technology is given and unchanged.

- Third, the resources are efficient and fully employed.

- Fourth, all the resources are not equally efficient in production of all goods.

4. Production Possibility Frontier Schedule and Curve

(a) It helps us to understand and solve the problem of what to produce and in what quantity.

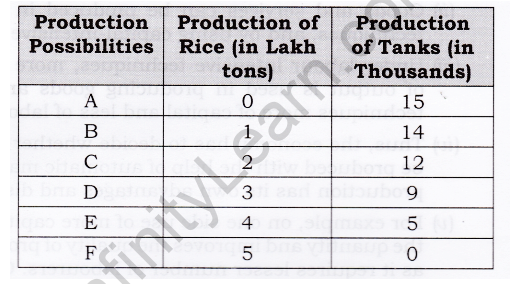

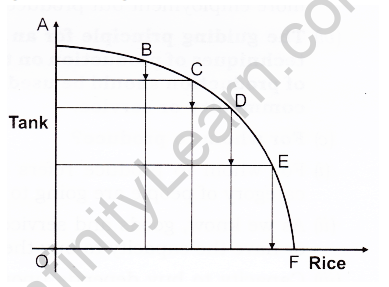

Let us for the sake of simplicity assume that with given resources and technology, an economy can produce only two goods, namely Rice and Tanks as shown in the production possibility schedule.

(b) By plotting the data, we get the following PP Curve:

In the given diagram, Tank is measured on vertical axis whereas Rice is measured on horizontal axis. If the economy decides to use all its resources in the production of Tanks, OA quantity of Tanks will be produced but Rice cannot be produced. On the other hand, if resources are devoted exclusively to the production of Rice, OF amount of Rice will be produced but no Tanks can be manufactured.

These two are extreme possibilities. In between, there are many other possibilities. Another alternative is that the economy devotes a part of its resources to the production of Tanks and a part to the production of Rice. In that case there can be different possibilities of production as is indicated by the points B, C, D and E. By joining points A, B, C, D, E and F of a curve, we get Production Possibility Curve.

(c) Full Employment and Underemployment Under PP Curve

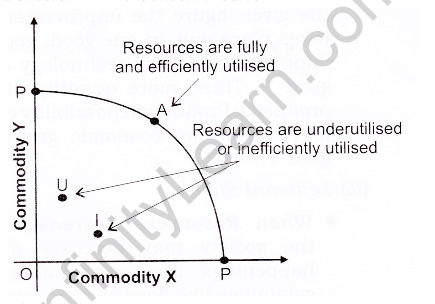

(i) Full Employment of Resources: It is represented along the PP-curve. The economy has to decide that which combination of good X and good Y should be produced. It means that the economy has to decide that how should resources be allocated in the production of good X and good Y. The desired allocation of the two goods must lie somewhere on the PP curve. For example, point A on the PP represents one such allocation.

(ii) Under Utilization of Resources: If resources are not fully and efficiently employed, may there be a problem of under utilization of resources. Under utilization of resources arises because of unemployment and inefficiency.

- The Problem of Unemployment: If the actual combination of two produced goods lies below the PP curve, it means that the resources are not fully employed. If the resources are fully employed, the combination must lie somewhere on the PP curve. For example, the combination ‘U’ below the PP curve represents unemployment, i.e., the resources are not fully utilized.

- The Problem of Inefficiency: Assuming that the resources are fully efficient, and if the actual combinations, say I, produced still lies below the PP curve, it means that resources are inefficiently employed. So, any combination that lies below the PP curve also indicates the problem of inefficient utilization of resources.

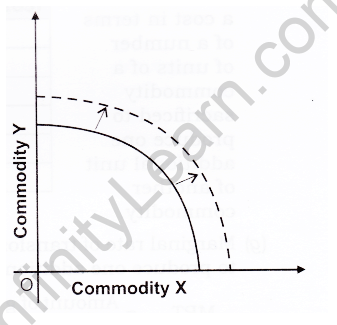

(d) Rightward and Leftward Shift of PP Curve

(i) Rightward Shift (When both Intercept Changes)

- When Resources Increase: Production possibility curve shows the combination of two pieces of goods which can be produced-by utilizing the resources efficiently. But, every economy tries to increase its resources so that more and more goods can be produced. PP curve is based on the assumption that the amount of resources in the economy is fixed. When resources are fixed, one or more goods can be produced only by sacrificing some quantity of the other good. We cannot produce more of both the goods. However, when resources increase, we can produce more pieces of both the goods.

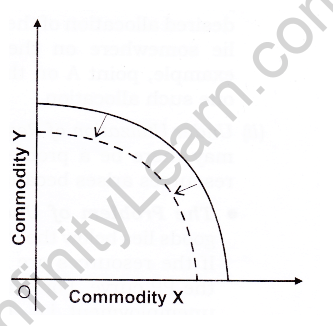

For example, Discovery of oil reserves in the GULF countries has caused a substantial shift to rightward in the PPC of these countries. - When Technology Changes: Generally, the change in technology is for the better. Better technology means that more quantities of both goods can be produced. In this situation also PP frontier shifts upwards.

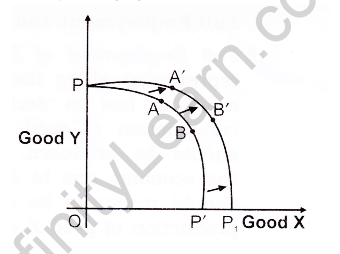

(ii) Rightward Shift (When One intercept Changes):

In the given figure the improvement in technology, takes place only in one good, good X. There is no improvement in the technology’ of producing the good Y. Thus, more quantity of good X can be produced. Production possibility curve PP’ expands to PP’ showing economic growth. Similarly for good Y.

(iii) Leftward Shift:

- When Resources Decrease: Resources with the society may decrease due to unusual happenings like earthquakes, war, natural calamities like floods etc. In such situations the production capacity of the country decreases, and the PP frontier shifts downwards.

(e) The concept of opportunity cost has occupied a very important place in economics. Modern economists have used the concept of opportunity cost in allocation of resources besides other fields.

Simply, opportunity cost means opportunity lost.

What is given up for getting something is called the opportunity cost of that thing. For instance, theoretically if a consumer has to forego 2 cups of tea for getting one glass of orange juice, opportunity cost of one glass of orange juice will be 2 cups of tea. Thus opportunity cost of any commodity is the amount of other goods which has been given up in order to produce that commodity. Alternatively opportunity cost of a given activity is the value of the next best activity.

(f) Marginal opportunity cost is an addition to a cost in terms of a number of units of a commodity sacrificed to produce one additional unit of another commodity.

(g) Marginal rate of transformation is the ratio of number of units of a good sacrificed to produce one additional unit of another commodity.

(h) PPC is concave to the point of origin because of increasing marginal opportunity cost (MOC). This behavior of the MOC is based on the assumption that all resources are not equally efficient in production of all goods. Rise in opportunity cost occurs when factors (resources) which are specialized or more adopted for production

of a particular good (say, guns), is transferred to the production of another good (say, rice) for which they are less productive or less specialized. Thus, transfer of resources from more productive to less productive uses indirectly means fall in their productivity, with the result more of such resources are needed to produce an additional unit of the other commodity. Thus marginal opportunity cost goes on increasing making the PP curve concave in shape.

5. Properties or Characteristics of Production Possibilty Curve

- PPC is downward sloping: The downward slope of PPC means that if the country wants to produce more of one good, it has to produce less quantity of the other goods.

- PPC is concave to the point of origin: Concave shape of PPC implies that slope of PPC increases. Slope of PPC is defined as the quantity of good Y given up in exchange for additional unit of good X.

6. Other shapes of PPC

(a) MOC Decreasing: PPC would be Convex to the point of origin, as shown below.

Microeconomics And Macroeconomics

Microeconomics

- Microeconomics studies the behaviour of individual economic units of an economy, like households, firms, individual consumers and producers etc.

- Its main instruments are demand and supply.

- It is also called ‘Price Theory’.

Macroeconomics

- Macroeconomics is that part of economic theory which studies the economy as a whole, such as national income, aggregate employment, general price level, aggregate consumption, aggregate investment, etc.

- Its main instruments are aggregate demand and aggregate supply.

- It is also called the ‘Income Theory’ or ‘Employment Theory’.

Words that Matter

1. Economy: Economy is a system which provides people with the means to work and earn a living.

2. Economics: Economics is about studying economic problems arising due to limited means (having alternative uses) in relation to unlimited wants.

3. Economic problem: Economic problem is a problem of choice involving satisfaction of unlimited wants out of limited resources having alternative uses.

4. Scarcity: Scarcity in economics is short supply in relation to the demand. Resources of the economy are scarce with the result that the economy can’t produce all that the society needs.

5. Economising of resources: It means that resources are to be used in such a manner that the maximum output is realised per unit of input. It also means optimum utilization of resources.

6. Central problem of an economy: The problem of making a choice among alternative uses of resources is known as basic or central problem of an economy.

7. What to produce: What to produce refers to a problem in which decision regarding which goods and services should be produced is to be taken.

8. How to produce: How to produce refers to a problem in which decision regarding which technique of production should be used.

9. For whom to produce: It refers to a problem in which decision regarding which category of people are going to consume a good, i.e., economically poor or rich.

10. Production: It is the process of transforming inputs (Raw material) into output (finished goods). So, production means creation of goods and services.

11. Consumption: It is a process of using up of goods and services to satisfy human wants.

12. Production possibility curve: It is a curve which depicts all possible combinations of two goods which can be produced with given resources and technology in an economy.

13. Production possibilities: It refer to different combinations of goods and services which an economy can produce from a given amount of resources and a given stock of technology.

14. Opportunity cost: Opportunity Cost of any commodity is the amount of other good which has been given up in order to produce that commodity. Alternatively opportunity cost of a given activity is the value of the next best activity.

15. Marginal opportunity: It is an addition to a cost in terms of a number of units of a commodity sacrificed to produce one additional unit of another commodity.

16. Marginal rate of transformation: It is the ratio of number of units of a good sacrificed to produce one additional unit of another commodity.

17. Microeconomics: The term ‘micro’has been derived from Greek word ‘MIKROS’means ‘small’. Microeconomics, therefore, studies the behaviour of individual economic units of an economy, like households, firms, individual consumers and producers etc.

18. Macroeconomics: It is that part of economic theory which studies the economy as a whole, such as national income, aggregate employment, general price level, aggregate consumption, aggregate investment, etc.