Table of Contents

This section focuses on key Past Adjustments in partnership accounts and the Guarantee of Profits to partners. These concepts are crucial for Class 12 CBSE Accountancy and frequently appear in exams.

Important Topics

- Past Adjustments in Partnership:

- Adjustments due to errors in the previous year’s profit distribution.

- Calculation methods for interest, salary, or share of profits.

- Guarantee of Profits to Partners:

- Scenarios where a partner is guaranteed a fixed amount of profit.

- Steps to adjust profits among partners.

The Class 12 Accountancy important questions are made by experts based on the latest CBSE books. It’s a good idea for students to go through these chapter-wise questions and answers. Doing this can really improve their marks in the upcoming board exams.

Also Check: CBSE Syllabus 2024

CBSE Class 12 Important Questions for Accountancy : Chapter wise

Volume 1

| Class 12 Solutions |

| Chapter 1- Company Accounts Financial Statements of Not-for-Profit Organizations |

| Chapter 2- Accounting for Partnership Firms- Fundamentals |

| Chapter 3- Goodwill- Nature and Valuation |

| Chapter 4- Change in Profit – Sharing Ratio Among the Existing Partners |

| Chapter 5- Admission of a Partner |

| Chapter 6- Retirement/Death of a Partner |

| Chapter 7- Dissolution of Partnership Firm |

Volume 1

| Class 12 Solutions |

| Chapter 8- Accounting for Share Capital |

| Chapter 9- Issue of Debentures |

| Chapter 10- Redemption of Debentures |

1. Past Adjustments Sometimes, after the final accounts of a firm have been closed, it is found that certain matters have been left out by mistake. In such cases, instead of altering the final accounts which have already been closed, the firm rectifies the error or omission by passing an adjustment entry in the beginning of the financial year. Such adjustments are called past adjustments as they relate to past period.

Steps to pass adjusting journal entry:

- Step 1 Calculate the amount already recorded.

- Step 2 Calculate the amount which should have been recorded.

- Step 3 Calculate the difference between Step 1 and Step 2.

- Step 4 Find out the partner who received excess and the partner who received short.

- Step 5 Pass the adjusting journal entry by debiting the partner who received excess and by crediting the partner who received short.

2. Guarantee A partner may be admitted into the firm with a guarantee of minimum profit, which means that if his share of profit is less than that of guaranteed profit, then he would be paid the guaranteed share of profit.

The deficiency (difference between guaranteed profit and actual profit) is borne by partner or partners who have guaranteed the profit in agreed ratio.

Different conditions regarding guarantee of profit are:

(i) Guarantee by the firm to a partner.

(ii) Guarantee by one partner to another partner.

(iii) Guarantee given by the partner to the firm.

(iv) Simultaneous guarantee by the firm to the partner and by the partner to the firm.

Steps Involved in the Distribution of Profits under Guarantee

Arrangement

Step 1 Calculate the actual share of profit/loss of guaranteed partner.

Step 2 Calculate the guaranteed amount.

Step 3 Calculate the amount of deficiency

Deficiency = Guaranteed Amount – Actual Share of Profit

Step 4 Distribute the deficiency among the guaranteeing partners in their guaranteeing ratio.

Step 5 Distribute the actual profits/losses among all the partners in their profit sharing ratio as if there is no guarantee arrangement.

Step 6 Recover share of deficiency (as per step 3) from the guaranteeing partners and give credit for the same to guaranteed partner.

Previous Years Examination Questions

3 Marks Questions

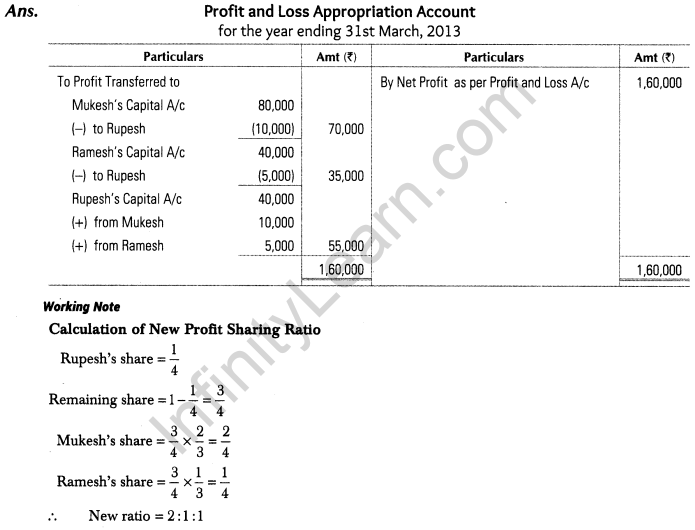

Q1. Mukesh and Ramesh are partners sharing profits and losses in the ratio of 2 : 1 respectively. They admit Rupesh as a partner with 1/4 share in profits with a guarantee that his share of profit shall be atleast Rs 55,000. The net profit of the firm for the year ending 31st March, 2013 was Rs. 1,60,000. Prepare profit and loss appropriation account.

(Compartment 2014)

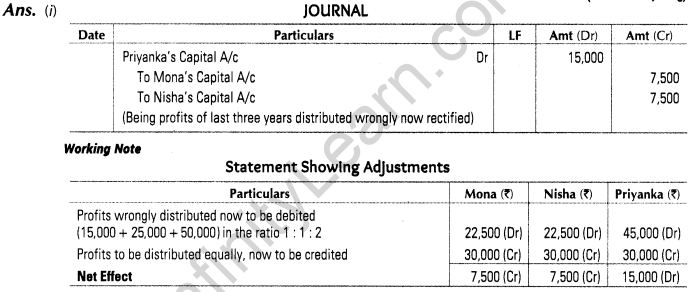

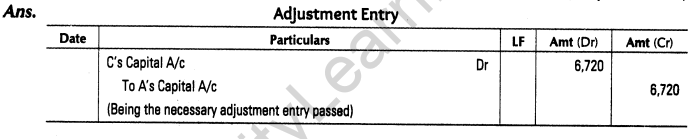

Q2. Mona, Nisha and Priyanka are partners in a firm. They contributed Rs. 50,000 each as capital three years ago. At that time, Priyanka agreed to look after the business as Mona and Nisha were busy. The profits for the past three years were Rs. 15,000, Rs. 15,000 and Rs. 50,000 respectively. While going through the books of accounts, Mona noticed that the profit had been distributed in the ratio of 1 : 1 : 2. When she enquired from Priyanka about this, Priyanka answered that since she looked after the business she should get more profit. Mona disagreed and it was decided to distribute profit equally retrospectively for the last three years.

(i) You are required to make necessary correction in the books of accounts of Mona, Nisha and Priyanka by passing an adjustment entry.

(ii) Identify the value which was not practised by Priyanka while distributing profits

(ii) Value not practised by Priyanka while distributing profits is (Any one)

(a) Honesty Priyanka has not shown honesty towards co-partners by not distributing profits as per the provision of Partnership Act.

(b) Transparency Priyanka has not shown transparency while distributing profits as per her wish and not communicating the same to other partners.

(c) Equity Priyanka has not shown equity in profit distribution.

(d) Team work Priyanka has not shown team work by hiding profit sharing ratio from other partners.

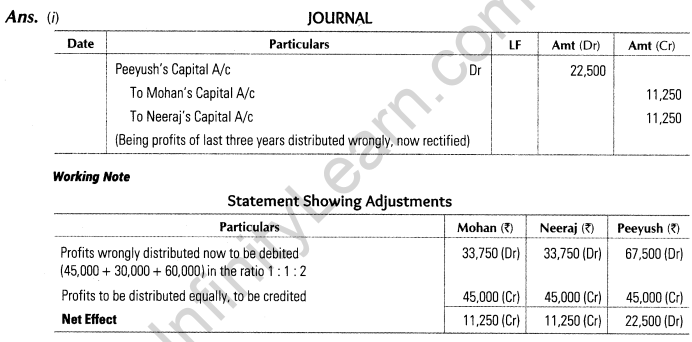

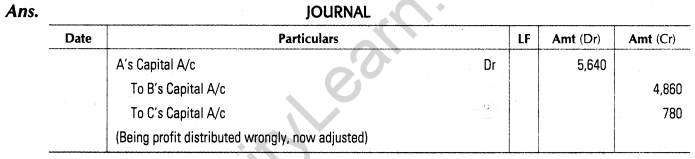

Q3. Mohan, Neeraj and Peeyush are partners in a firm. They contributed Rs. 75,000 each as capital three years ago. At that time, Peeyush agreed to look after the business as Mohan and Neeraj were busy. The profits for the past three years were Rs. 45,000, Rs. 30,000 and Rs. 60,000 respectively. While going through the books of accounts, Mohan noticed that profit had been distributed in 1 : 1 : 2 ratio. When he enquired from Peeyush about this, Peeyush answered that since he looked after the business he should get more profit. Mohan disagreed and it was decided to distributed profits equally with respectively effect for the last three years.

(i) You are required to make necessary corrections in the books of accounts of Mohan, Neeraj and Peeyush by passing an adjustment entry.

(ii) Identify the value which is being ignored by Peeyush. (All India 2013; VBQ)

(ii) Value not followed by Peeyush while distributing profits is (Any one)

(a) Honesty Peeyush has not shown honesty towards co-partners by not distributing profits as per Partnership Act.

(b) Transparency Peeyush has not shown transparency while distributing profits as per his wish and not communicating the same to other partners.

(c) Equity Peeyush has not shown equity in profits distribution.

(d) Team work Peeyush has not shown team work by hiding profit sharing ratio from other partners.

4 Marks Questions

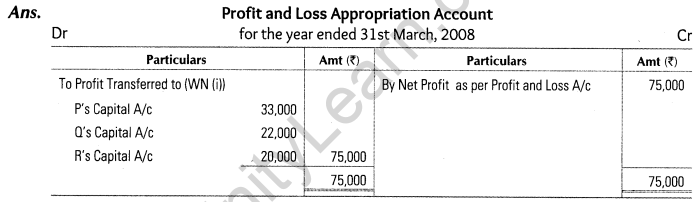

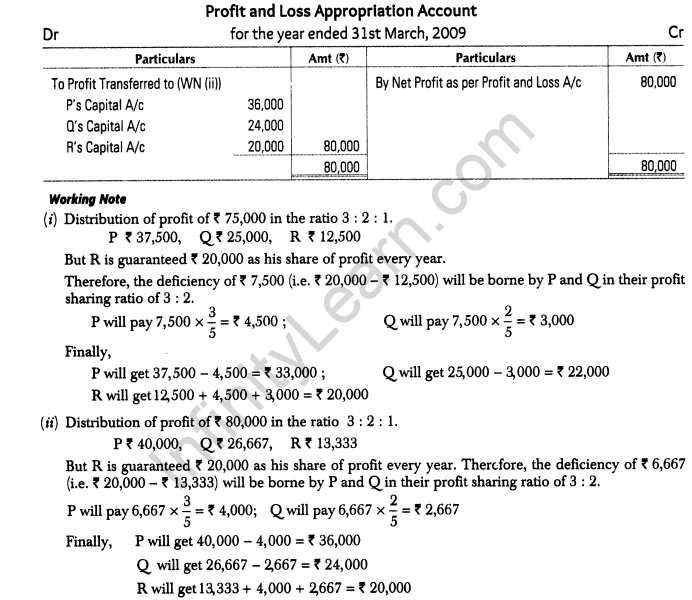

4. P,Q and R are partners sharing profits in the ratio of 3 : 2 : 1. However, R is guaranteed Rs. 20,000 as his share of profits every year. Deficiency if any would be borne by the other partners. The profits for the two years ending 31st March, 2008 and 31st March, 2009 had been Rs. 75,000 and Rs. 80,000 respectively. Show the profit and loss appropriation account for the two years.

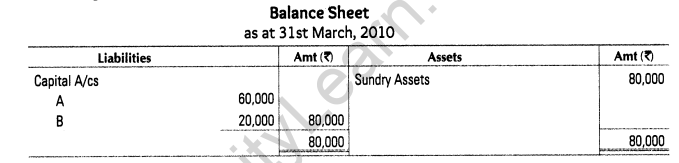

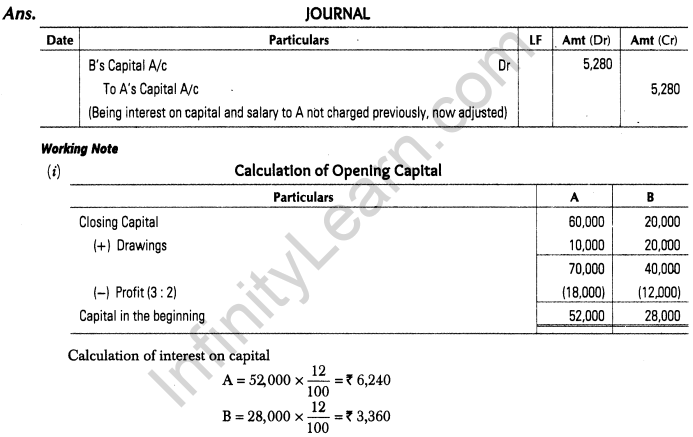

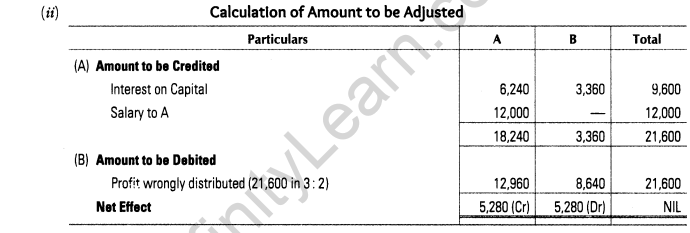

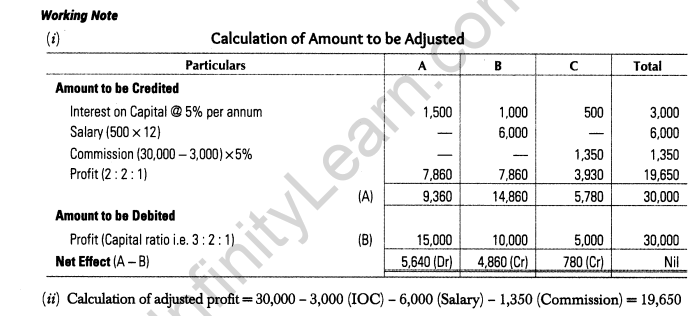

Q5. A and B are partners in a firm sharing profit and losses in the ratio of 3 : 2. The following was the balance sheet of the firm as at 31st March, 2010.

The profits Rs. 30,000 for the year ended 31st March, 2010 were divided between the partners without allowing interest on capital @ 12% per annum and salary to A @ Rs. 1,000 per month. During the year, A withdrew Rs. 10,000 and B Rs. 20,000.

Pass the necessary adjustment journal entry and show your working clearly. (Delhi 2011)

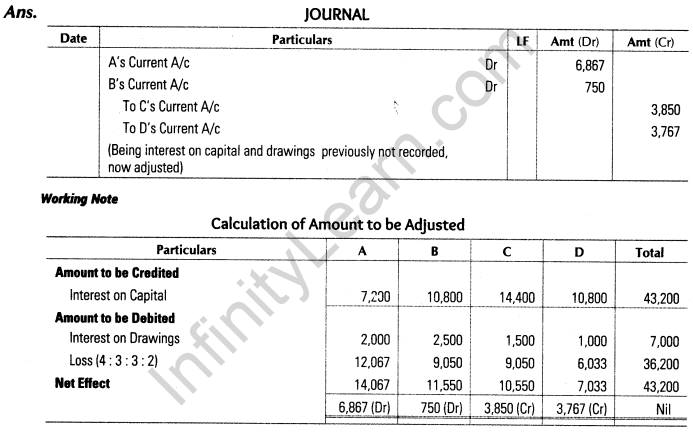

Q6. A, B, C and D are partners sharing profits and losses in the ratio of 4 : 3 : 3 : 2. Their respective fixed capitals on 31st March, 2010 were Rs. 60,000, Rs. 90,000, Rs. 1,20,000 and Rs. 90,000 respectively. After preparing the final accounts for the year ended 31st March, 2010, it was discovered that interest on capital @ 12% per annum was not allowed and interest on drawings amounting to Rs. 2,000, Rs. 2,500, Rs. 1,500 and Rs. 1,000 respectively was also not charged.

Pass the necessary adjustment journal entry showing your working clearly. (All India 2011)

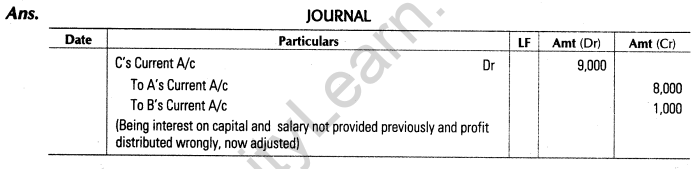

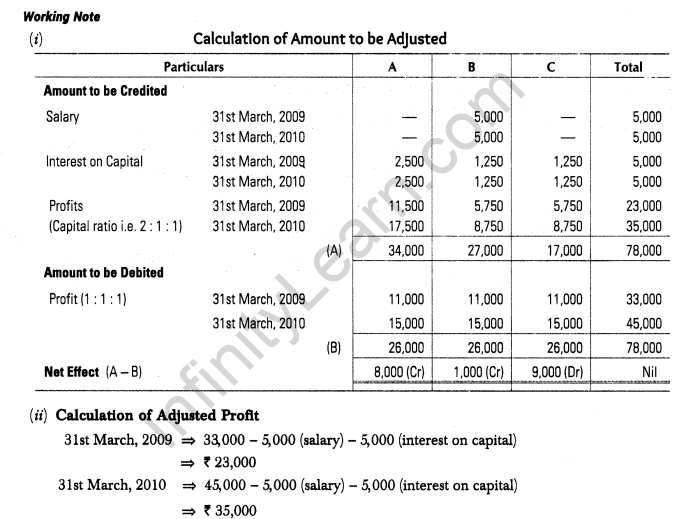

Q7. A, B and C were partners in a firm. On 1st April, 2008, their fixed capitals stood at Rs. 50,000, Rs. 25,000 and Rs. 25,000 respectively.

As per the provisions of the partnership deed

(i) B was entitled for a salary of Rs. 5,000 per annum.

(ii) All the partners were entitled to interest on capital at 5% per annum.

(iii) Profits were to be shared in the ratio of capitals.

The net profit for the year ending 31st March, 2009 of Rs. 33,000 and 31st March, 2010 of Rs. 45,000 was divided equally without providing for the above terms.

Pass an adjustment journal entry to rectify the above error. (All India 2011)

Q8. A, B and C were partners. Their capitals were Rs. 30,000, Rs. 20,000 and Rs. 10,000 respectively. According to the partnership deed, they were entitled to interest on capital @ 5% per annum. In addition, B was also entitled to draw a salary of Rs. 500 per month. C was entitled to a commission of 5% on the profits after charging the interest on capitals but before charging the salary payable to B. The net profits for the year were Rs. 30,000 distributed in the ratio of their capitals without providing for any of the above adjustments. The profits were to be shared in the ratio of 2 : 2 :1. Pass the necessary adjustment entry showing the working clearly. (Delhi 2010)

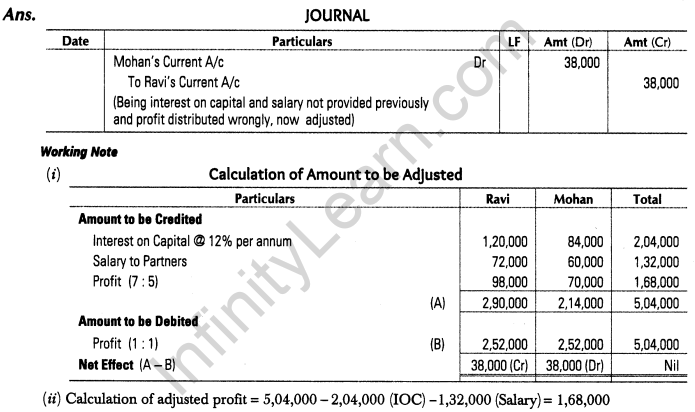

Q9. Ravi and Mohan were partners in a firm sharing profits in the ratio of 7 : 5. Their respective fixed capitals were Ravi Rs. 10,00,000 and Mohan Rs. 7,00,000.

The partnership deed provided for the following

(i) Interest on capital @ 12% per annum.

(ii) Ravi’s salary Rs. 6,000 per month and Mohan’s salary Rs. 60,000 per year.

The profit for the year ended 31st March, 2007 was Rs. 5,04,000 which was distributed equally, without providing for the above. Pass an adjustment entry. (Delhi 2008)

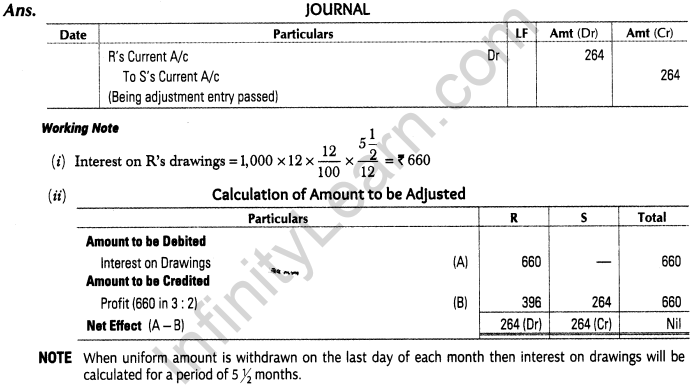

Q10. R and S were partners in a firm sharing profits in the ratio of 3 : 2. Their respective fixed capitals were R Rs. 10,00,000 and S Rs. 15,00,000. The partnership deed provided the following

(i) Interest on capital @ 10% per annum.

(ii) Interest on drawings @ 12% per annum.

During the year ended 31st March, 2007, R’s drawings were Rs. 1,000 per month drawn at the end of every month and S’s drawings were Rs. 2,000 per month drawn in the beginning of the every month. After the preparation of final accounts for the year ended 31st March, 2007, it was discovered that interest on R’s drawings were not taken into consideration.

Calculate interest on R’s drawings and give necessary adjustment entry for the

The profit for the year ended 31st March, 2007 was Rs. 2,78,000. Which was distributed equally without treating the above adjustments.

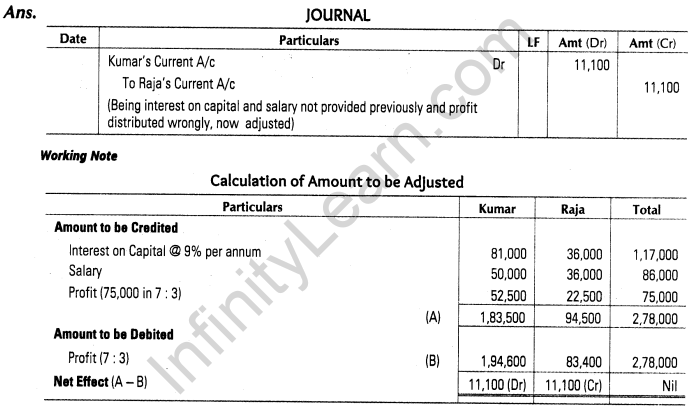

Q11. Kumar and Raja were partners in a firm sharing profits in the ratio of 7 : 3. Their fixed capitals were Kumar ? 9,00,000 and Raja ? 4,00,000. The partnership deed provided for the following but the profit for the year was distributed without providing for:

(i) Interest on capital @ 9% per annum.

(ii) Kumar’s salary Rs. 50,000 per year and Raja’s salary Rs. 3,000 per month. Pass the adjustment entry. (All India 2008)

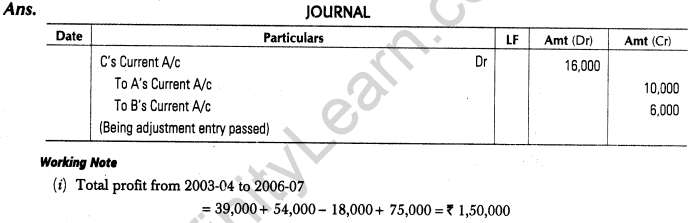

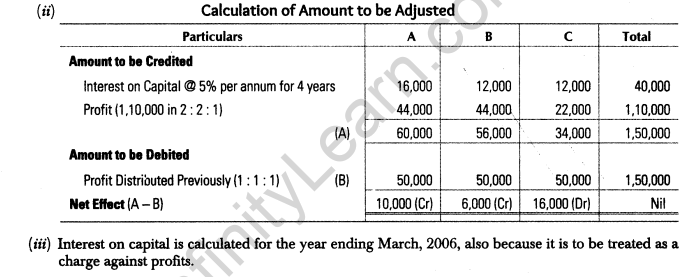

Q12. A, B and C were partners in a firm. They had no partnership deed. They had been in business for 4 years and their profit and loss for this period was, year ended March 2004 Rs. 39,000, March 2005 Rs. 54,000, March 2006 Rs. 18,000 (loss) and March 2007 Rs. 75,000. During the year 2007-08, they agreed to share profits and losses in the ratio of 2 : 2 : 1 with retrospective effect from the year 2003-04. It was also decided that an interest (charge) of 5% per annum was to be provided on capitals (fixed). Their capitals were Rs. 80,000, Rs. 60,000 and Rs. 60,000 respectively. Pass a single adjustment entry to adjust the capital accounts of the partners. (All India 2008)

6 Marks Questions

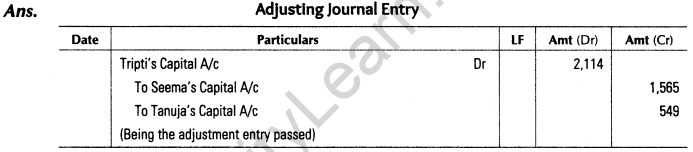

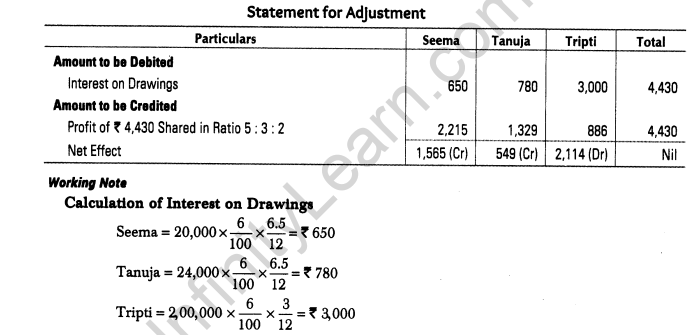

Q13. Seema, Tanuja and Tripti were partners in a firm trading in garments. They were sharing profits in the ratio of 5 : 3 : 2. Their capitals on 1st April, 2012 were Rs. 3,00,000, Rs. 4,00,000 and Rs. 8,00,000 respectively. After the flood in Uttarakhand, all partners decided to help the flood victims personally.

For this, Seema withdrew Rs. 20,000 from the firm on 15th September, 2012. On the same date, Tanuja instead of withdrawing cash from the firm, took garments amounting to Rs. 24,000 from the firm and distributed those to the flood victims. On the other hand, Tripti withdrew Rs. 2,00,000 from her capital on 1st January, 2013 and provided a mobile medical van in the flood affected area.

The partnership deed provides for charging interest on drawings @ 6% per annum. After the final accounts were prepared, it was discovered that interest on drawings had not been charged. Give the necessary adjusting journal entry and show the working notes clearly. Also, state any two values which the partners wanted to communicate to the society. (Modified; All India 2014)

The values which partners wanted to communicate to the society are

(i) Concern and care towards flood victims By donating garments and providing medical facilities to the flood victims partners have shown care and concern towards them.

(ii) Doing your best and compassion Partners have done their best and have shown compassionate behaviour by helping the flood victims.

NOTE It has been assumed that Tanuja has made drawings on the same date as of Seema.

Q14. A, B and C were partners. They started business in one of the remote tribal areas of Odisha. They were interested in the development of the tribal community by providing good education and health.

On 31st March, 2013, after making adjustments for profits and drawings their capitals were A – Rs. 4,00,000, B – Rs. 3,00,000 and C Rs. 2,00,000. The drawings of the partners were A – Rs. 4,000 per month, B – Rs. 3,000 per month and C – Rs. 2,000 per month.

The profit of the firm for the year ended 31st March, 2013 was ? 6,00,000. Subsequently it was found that the interest on capital @ 6% per annum due, had been omitted.

Showing your working notes clearly, pass necessary adjustment entry for the above. Also, identify any two values highlighted in the above question.

(Compartment 2014)

Values highlighted in the above question are

(i) Development of remote tribal area, by providing employment opportunities.

(ii) Equity, even though capital contributions are unequal, still the partners are sharing profits equally, thereby promoting harmony and brotherhood.

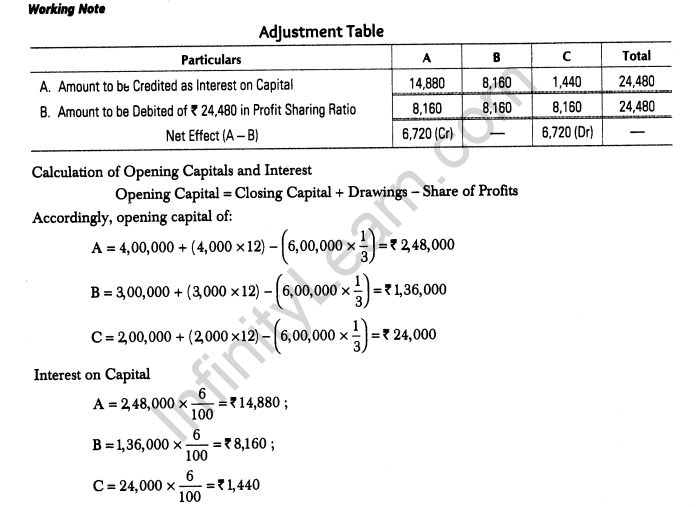

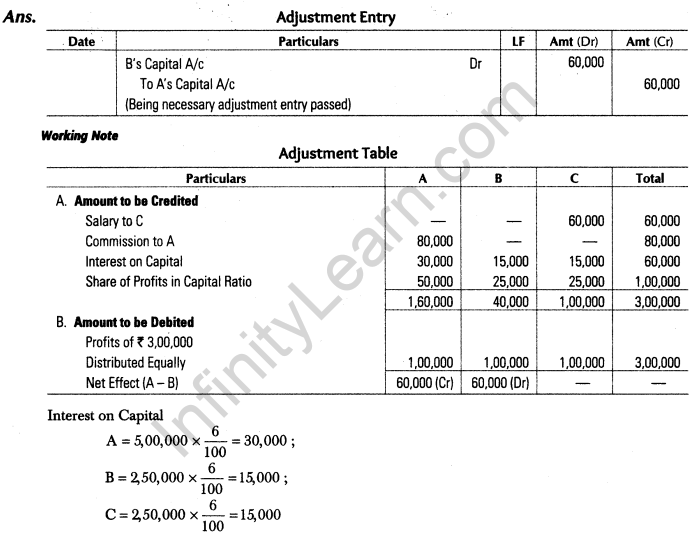

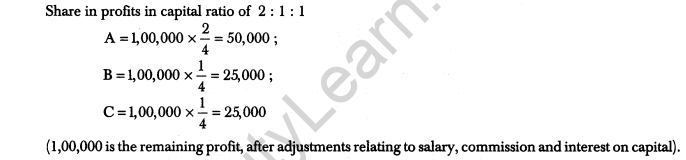

Q15. A, B and C were partners in a firm. On 1st April, 2012 their capitals stood as Rs. 5,00,000; Rs. 2,50,000 and Rs. 2,50,000 respectively.

As per provisions of the partnership deed

(i) C was entitled for a salary of Rs. 5,000 per month.

(ii) A was entitled for a commission of Rs. 80,000 per annum.

(iii) Partners were entitled to interest on capital @ 6% per annum.

(iv) Partners will share profits in the ratio of capitals.

Net profit for the year ended 31st March, 2013 was Rs. 3,00,000 which was distributed equally, without taking into consideration the above provisions. Showing your working clearly, pass necessary adjustment entry for the above. (Compartment 2014)

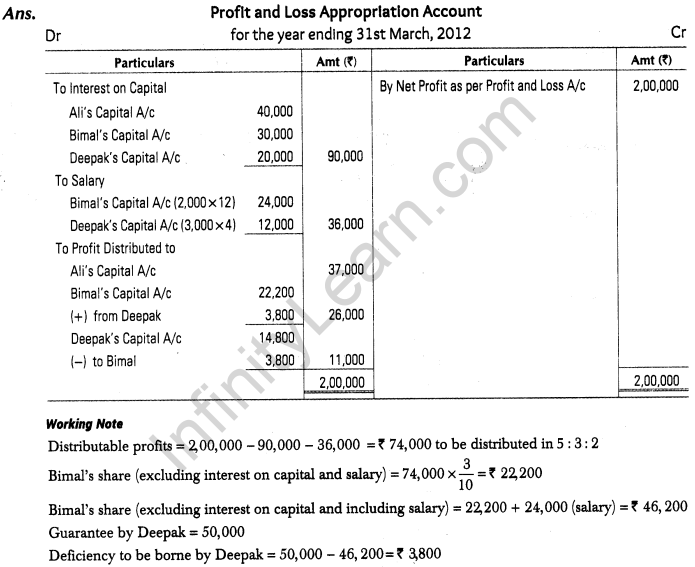

Q16. Ali, Bimal and Deepak are partners in a firm. On 1st April, 2011 their capital accounts stood at Rs. 4,00,000, Rs. 3,00,000 and Rs. 2,00,000 respectively. They shared profits and losses in the ratio of 5 :3 : 2 respectively. Partners are entitled to interest on capital @ 10% per annum and salary to Bimal and Deepak @ 12,000 per month and Rs. 3,000 per quarter respectively as per the provisions of the partnership deed.

Bimal’s share of profit (excluding interest on capital but including salary) is guaranteed at a minimum of Rs. 50,000 per annum. Any deficiency arising on that account shall be met by Deepak. The profits of the firm for the year ended 31st March, 2012 amount to Rs. 2,00,000. Prepare profit and loss appropriation account for the year ended on 31st March, 2012. (Delhi 2013)

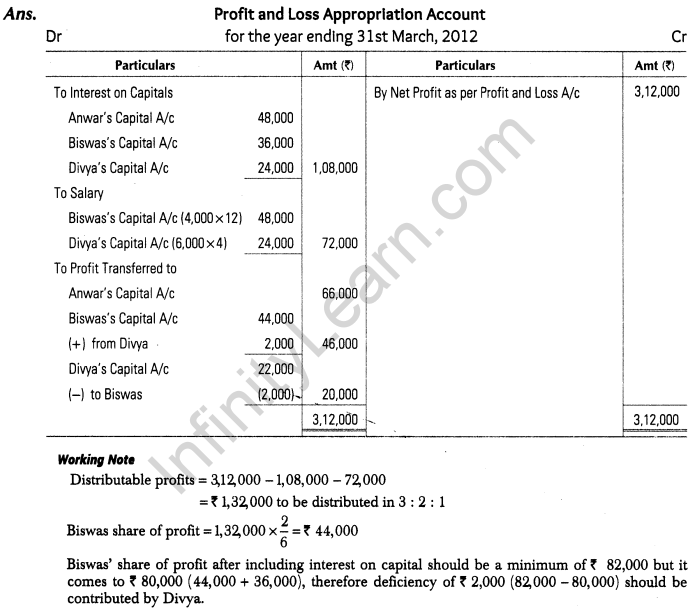

Q17. Anwar, Biswas and Divya are partners in a firm. Their capital accounts stood at Rs. 8,00,000, Rs. 6,00,000 and Rs. 4,00,000 respectively on 1st April, 2011. They shared profits and losses in the ratio of 3 : 2 :1 respectively. Partners are entitled to interest on capital @ 6% per annum and salary to Biswas and Divya @ Rs. 4,000 per month and Rs. 6,000 per quarter respectively as per the provisions of partnership deed.

Biswas’s share of profit (including interest on capital but excluding salary) is guaranteed at a minimum of ?82,000 per annum. Any deficiency arising on that account shall be met by Divya. The profits for the year ended 31st March, 2012 amounted to Rs. 3,12,000. Prepare profit and loss appropriation account for the year ended 31st March,2012. (Deihi 2013)

Important Questions for CBSE Class 12 Accountancy FAQs

Was Class 10 maths paper tough in 2023?

The difficulty of the Class 10 maths paper in 2023 varied for different students.

How was CBSE maths paper 2023?

The CBSE maths paper in 2023 had mixed opinions on its difficulty.

Will CBSE 2023 be easy for Class 10?

The ease of CBSE exams in 2023 for Class 10 varied across subjects.

How was the Class 10 maths paper in 2023?

The Class 10 maths paper in 2023 had differing opinions regarding its level of difficulty.

Is CBSE releasing the answer key for 2023?

CBSE's release of the answer key for exams in 2023 varied and wasn't consistent for all subjects.